- Home

- International Symposia

- Research Projects

- Value, Money And Credit In Ancient Greek Market Economy

- Object and Scope of Research

- The Origin Of Coinage: Nature, Function and Value of Money in Archaic Greece (Abstract)

- The Origin Of Coinage: Nature, Function and Value of Money in Archaic Greece

- Preface, Table of contents and Introduction of Value and Knowledge, The Philosophy of Economy in Classical Anriquity)

- Aristotle's Individualistic Foundation of Political Society: Self-Interest and Utility (Chapter 2 of the Value and Knowledge)

- The Utility Theory of Value and Money (Chapter 4 of the Value and Knowledge)

- Knowledge as the Ultimate Asset of Wealth, The Knowledge Theory of Value (Chapter 6 of Value and Knowledge

- The Nature of Interest (Appendix A of Value and Knowledge)

- The Stable Cyclicity of Natural Equilibrium (Appendix C of Value and Knowledge)

- On the value and Stability of Currency (Appendix E of Value and Knowledge)

- The Platonic Foundation of Marginalism, the Paradox of Wealth and the Infinite Desire for Power (Appendix I of value and Knowledge)

- Pleasure as Felt restoration and as Unimpeded Activity- The Disutility and Utility Factors in Human Action (Appendix J of Value and Knowledge)

- "Αναγκαία Τροφή"

- Αξία Τροφής και Αντιπληθωρισμός στην Κλασσική Αρχαιότητα

- The Platonic Credit Economy and Fiat Money

- Knowledge as the Ultimate Asset of Power

- Το Χρηματοπιστωτικό Σύστημα στην Κλασσική Αρχαιότητα: Σταθερότητα Αξίας Χρήματος και Τιμών

- Νέα Μελέτη για την Οικονομία της Αγοράς στην Κλασσική Αρχαιότητα

- Η Τεχνική της Πρόβλεψης, η Λογική της Ανάπτυξης και η Αρχαία Ελληνική Σκέψη

- The Emergence of Reason from the Spirit of Mystery

- Η Γέννηση του Λογου από το Πνεύμα του Μυστηρίου

- The Logical Order of Presocratic Chronology

- Preface

- Origin and Nature of Early Pythagorean Cosmogony

- Religion and Mystery, Preface and table of Contents

- Baubo and Iacchus (Religion and Mystery, Chapter 7)

- Zeus, Zagreus, Aidoneus (Chapter 8 of Religion and Mystery)

- Note on Colour Symbolism

- Project Description

- The Law of Inviolable Justice: Mechanism of Self-Sustainable Cosmic Order

- Ὁ Μονισμὸς τοῦ Σκότους καὶ ὁ Δυισμὸς Πέρατος - Ἀπειρίας

- The Religious and Social Policies of the Delphic Oracle

- Μίασμα and Κάθαρσις

- Divination and the Divine Order

- Αρχή Περιόδου: Beginnings in Cyclic Processes

- Preclassical Orphism

- The Monism of Darkness and the Dualism of Limit and Indeterminacy

- On Greek Rationalism

- First Principles and the Beginning of Philosophy

- First Principles and the Beginning of Philosophy

- Η Αρχή του Όντος: Λόγος περί Πρώτων Αρχών στην Πρώιμη Ιωνική Φιλοσοφία

- Χρονολόγιο Πρώιμης Φιλοσοφίας: Αρχαική Εποχή

- Τα Ύδατα της Στυγός: Φύση και Νόημα ενός Τόπου Παρουσίας του Αρχέγονου Υγρού

- Ο Ηρακλείτειος Κόσμος

- Παρμενίδης: Ο Μονισμός του Είναι και ο Δυισμός του Γίγνεσθαι

- Προβλήματα Αρχαικής Φυσιολογίας: ο Νόμος του Μονισμού και η Αρμονία του Δυισμού. Από τον Θαλή δια του Πυθαγόρα στον Ηράκλειτο

- Λογόμυθος Ελληνικής Κοσμογονίας και Σωτηριολογίας

- Αναστάσιμο Εξάγγελμα

- Αισχύλου Θεολογούμενα Διονυσιακά

- Η Αρχή του Όντος

- Μεταφυσική και Μετασυμβολική

- Αναστάσιμη Δοξολογία Ελληνισμού

- Σημείωμα για τα Ελευσίνια Μυστήρια

- Derveni Papyrus

- Η Σημασία και το Σκάνδαλο του Παπύρου του Δερβενίου

- In Search of the Author and of a Second Book

- Για τον Πάπυρο του Δερβενιού και το σκάνδαλο της έκδοσής του

- Η 'Εκδοση του, τα Κλεψίτυπα και οι …Αντιγραφές

- Τα Κρυφά, τα Φανερά και τα Προφανή

- Οι Δικαιολογίες και η …Ταμπακέρα

- Το Αληθινό Χρονικό της Ευρεσης του Παπύρου του Δερβενίου

- O Πάπυρος, οι Περγαμηνές και η Ουσία

- Απόστολος Πιερρής, Φιλόσοφος με… αιτία

- The Phallic Helios of the Derveni Papyrus

- Examining the Derveni Papyrus with the Brigham Young Universsity Digital Imaging Team

- Examining the Derveni Papyrus with the Brigham Young Universsity Digital Imaging Team 2

- Inspired Voice and natural Philosophy in the DP

- DP and the Question of Authorship: an Anaxagorean and indeed Archelaus?

- The Origin of Allegory: Philosophical Logos, "Mixed" Theology and the Iranian Connection

- On the General Significance for Greece of the derveni papyrus Affair

- Η Σημασία και το Σκανδαλο του Παπύρου του Δερβενίου 2

- The Making of a Miracle: Athenean Golden Age

- The Way of Things: Parallel ways in Classical Greek and Chinese Philosophy

- Plan for a Sino-Greek Classical Philosophy Conference

- Original Planning For A Sino-Greek Classical Philosophy Meeting And Research Project

- Further Ideas On Sino-Greek Classical Philosophy Forums

- Beijing, Summer 2009 Conference On Classical Chinese And Greek Philosophy

- Socrates and Confucius: Tradition, Innovation and Value Redefinition in Higher Cultures of Strong Identity

- Project On Islam And Classical Helinism In World History

- Geopolitics and the Vector of History: Unipolar Systems and World Hegemony

- History and Theory of Geopolitical Dominance

- Athens, Rome and the American Imperium

- Knowledge, Science and Ancient Greek Philosophy in an Age of Transition

- Βίοι Παράλληλοι of World-Powers in History: Athens and USA

- The Triple Axis against USA in 2003

- Bulgaria's Lesson on Euro-Madness

- Μονοπολική Στρατηγική and "Smart" Power

- Το Κεντρικό Σύστημα της Ιστορίας, 2η έκδοση - Ο Θάνατος της Ευρώπης και η Ανανέωση του Κόσμου

- Hellinism And History

- Στοιχείωσις Οντολογική της Απόλυτης Αντίφασης Ελληνισμού και Ευρωπαισμού

- Δωρική Σπάρτη, Μάνη και η Επανάσταση του ¨21 (Η Μορφή της Ελληνικής Ιστορίας και η Αμορφία του Νεοελληνικού Κράτους)

- Επικαιρικά, Διαχρονικά και Αιώνια. Ποιοί Είμαστε; Που Πάει ο Κόσμος; Χρησμοί εξ Αιωνιότητος για την Ταυτότητά μας και το Άνυσμα της Ιστορίας

- Η Ανθρώπινη Ταραχή

- Κοσμικές Τάξεις

- Η Κατάρρευση του Μεταλλικού Συστήματος (1274 - 1184 π.Χ.)

- Ελληνισμός και Χρόνος. Παρελθόν, Παρόν και Μέλλον του Θαύματος της Αποκάλυψης στην Ιστορία

- Η Κοσμοιστορική Σημασία της Α' Χιλιετίας π.Χ. Από την Κατάρρευση του Μεταλλικού Συστήματος Ισχύος στην Ίδρυση της Ρωμαικής Αυτοκρατορίας - Στοχασμοί Βάσης για την Διαλεκτική Αιωνιότητας και Χρόνου στην Ιστορία

- Στοχασμοί για την Κατάσταση του Κόσμου και τον Ιό

- Αφορισμοί για μια Ανατομία του Φόβου

- Το Τέλος του Ευρωπαικού Πολιτισμού

- Σημείωση περί Κορονοιού

- Οι Θεοί του Ελληνισμού, τα Είδωλα της Ευρώπης και η Πονηρία του Νεοελληνικού Συστήματος

- Πολιτισμοί. Στοχασμοί πάνω στο Κλασσικό, το Βυζαντινό και το Ευρωπαικό

- Ο Βαρβαρισμός της Νεωτερικότητας (Ευρωπαικής και Νεοελληνικής) και το Κλασσικό

- Θανάσιμα και Αναστάσιμα

- Η Πνοή του Κάλλους Πνεύμα Θεού

- Το Κεντρικό Σύστημα της Ιστορίας, 2η έκδοση - Ο Θάνατος της Ευρώπης και η Αννέωση του Κόσμου

- Σύνοψις Αληθούς Γνώσης και Πρόγνωσης

- Σπάρτη και Αθήνα

- Logos in Ancient Greek Philosophy and Christianity

- Θεάνθρωπος: Christological Aetia

- Η Γέννηση του Θεού για την Νέα Χιλιετία

- Epiphanies: Eternity in Time and the Teleology of Creation

- Συλλαβαί Θείας Φιλοσοφίας

- Logos as Ontological Principle of Reality

- Θεάνθρωπος: Αίτια Δογματικά Χριστολογίας

- Ελληνισμός, Ορθοδοξία και Σύγχρονος Κόσμος - κατά της Προσωπολατρείας της Νεοορθοδοξίας

- Η Πάλη των Θρησκειών στην Ρωμαική Αυτοκρατορία (Τέλος του 1ου π.Χ. αι. - Αρχές του 4ου μ.Χ.)

- Prolegomena to the Enigma of the Johannine Prologue: an Inquiry into Ancient Philosophical Syncretism

- Prolegomena to the Enigma of the Johannine Prologue (published in "KRONOS", V, 1916)

- Αναστάσιμοι Στοχασμοί

- Η Εκκλησία, το Έθνος και η Καιρική Μωρία

- Θανάσιμα και Αναστάσιμα

- Η Πνοή του Κάλλους Πνεύμα Θεού

- Greco-Egyptian Interaction in the Ancient World

- Myth as Archetype

- Stoic Studies

- Aristotelian Studies

- Theraean Inscriptions Project

- Platonic and Metaphysical Studies

- Roads to Excellence

- The Metaphysics of Politics

- Things and Predication

- Η Θέσις του Πλατωνικού Τιμαίου στην Ιστορία του Ελληνικού Δυισμού

- Ο Λόγος ως Αρχή του Όντος

- On the Notion of Infinity and the Regressus ad Infinitum in Metaphysics (working copy)

- On the Notion of Complete Determination

- Concerning Determinants and an alleged Element in Proper Predication

- On Existence

- Some Comments on Strawson's "The Asymmetry of Subjects and Predicates"

- Concerning the Nature and Structure of Determinants

- Plato's Theory of Forms and the Doctrine of Imitation

- The Theology of Iamblichus

- Introductory remarks on Neoplatonic Metaphysics and Damascius' De Primis Principiis

- Commentary on the Beginning of Damascius' De Primis Principiis

- Οι Ιδέες-Αριθμοί του Πλάτωνα και το "τί ην είναι" του Αριστοτέλη

- On Indivisible Lines and Temporal Atoms: The Problem of Space-Time Continuum in Ancient Greek Thought

- Inquiries concerning Classical Values and Virtues

- Antiquarian Investigations

- Χρονογραφικά Σύμμεικτα

- Περί Γενεάς

- Περί Ηλικιών Βίου

- Περί της Σωματικής Αρετής

- Περί Χαρίτων και Ωρών

- Περί Χλαμύδος

- On Depilation: Body Cosmetics in Classical Antiquity

- On Asclepius' Parentage, Birthplace and Cult-Localization

- On the Sacred Route from Delos to Delphi and the Phlegyans

- On Oechalia

- Κάρνεια Ιερομηνιακά

- On the Athenian Hieropoioi

- ΟΙΝΟΛΟΓΙΚΑ: On Wine and Vineous Liquors

- Η Δελφική Ανεξαρτησία και ο Α' Ιερός Πόλεμος

- Χώρος και Ιστορία: Χωρολογικά Αίτια του Ιστορικού Ρυθμού

- Πρόλογος - Εισαγωγή

- Γενικές Αρχές Δυναμικής Συστημάτων - Δύναμις, Δικαίωμα, Δίκαιον

- Ο Βασικός Ρυθμός του Ιστορικού Γίγνεσθαι

- Ολοκληρώσεισ Πεδίων Δυνάμεων στην Ιστορία

- Η Ατελής Περσική Αυτοκρατορία

- Η Ατελέσφορος Ηγεμονική Άνοδος και η Αποτυχία των Αθηνών

- Το Ρωμαικό Imperium και Οικουμενική Αυτοκρατορία

- Γεωπολιτική Δομή και Μή Ολοκληρώσιμο του Ευρωπαικού Χώρου

- Τροπή των Χιλιετιών: Renovatio Mundi

- Φυσικά Συστήματα και Ελευθερία, Ελληνικό Πνεύμα και Renovatio Mundi

- Η Οθωμανική Ολοκλήρωσις

- Οι Απόπειρες Γαλλικής Ενοποιήσεως της Ευρώπης

- Οι Απόπειρες Γερμανικής Ολοκληρώσεως της Ευρώπης

- Πηγές των Εικόνων

- Το ΒαλκανοΜικρασιατικό Γεωπολιτικό Πεδίο και η Ευρύτερη Δυναμική του

- Διακρατικές Διενέξεις και Διαιτησία

- Περιφερειακά Πεδία Δυνάμεων: Ευρώπη

- Γεωστρατηγική των ΕλληνοΤουρκικών Σχέσεων μετά την Κρίσι των Ίμια

- Ανατομία της Ελληνικής Στρατηγικής 'Ηττας

- Ευρωπαική Ένωσις και ΕλληνοΤουρκικαί Σχέσεις - Ι

- Ευρωπαική Ένωσις και ΕλληνοΤουρκικαί Σχέσεις - ΙΙ

- Ευρωπαική Ένωσις και ΕλληνοΤουρκικαί Σχέσεις - ΙΙΙ

- Ευρωπαική Ένωσις και ΕλληνοΤουρκικαί Σχέσεις - ΙV

- Ευρωπαική Ένωσις και ΕλληνοΤουρκικαί Σχέσεις - V

- Ευρωπαική Ένωσις και ΕλληνοΤουρκικαί Σχέσεις - VI

- Ευρωπαική Ένωσις και ΕλληνοΤουρκικαί Σχέσεις - VII

- Ευρωπαική Ένωσις και ΕλληνοΤουρκικαί Σχέσεις - VIII

- State-Religion Relationships in the Balkan-Asia Minor Geopolitical Field

- Ο Μύθος των Ηπείρων και η Πραγματικότητα των Γεωπολιτικών Περιφερειών

- Ανατολική Μεσόγειος και το Κεντρικό Σύστημα της Ιστορίας

- Το Κεντρικό Σύστημα της Ιστορίας, 2η έκδοση - Ο Θάνατος της Ευρώπης και η Ανανέωση του Κόσμου

- Ανατολική Μεσόγειος και το Κεντρικό Σύστημα της Ιστορίας, Γ΄ Έκδοση: Θουκυδίδου Μηλιακά

- Byzantine Inquiries

- Η Δυτική Πολιτική της Βυζαντινής Αυτοκρατορίας και οι Σχέσεις Ανατολικής και Ρωμαικής Εκκλησίας (1041 - 1053 μ.Χ.)

- Η Δυτική Πολιτική της Βυζαντινής Αυτοκρατορίας και οι Σχέσεις Ανατολικής και Ρωμαικής Εκκλησίας (1054 - 1064 μ.Χ.)

- Θεοδώρου του Σμυρναίου, Λόγος περί της Εκπορεύσεως του Αγίου Πνεύματος

- Νικήτα Ακομινάτου Χωνιάτη, Απορίαι και Λύσεις περί της Εκπορεύσεως του Αγίου Πνεύματος

- Νικήτα Ικονιαίου του Σείδου Λόγος σχεδιασθείς προς Ρωμαίους εναντίον των Πρωτείων του Πάπα και περι της Εκπορευσεως του Αγίου Πνεύματος Πρωτ

- Ελληνισμός και Βυζάντιο

- Μορφή στην Ιστορία: ο Ελληνισμός και η Μοίρα του Βυζαντίου

- Το Μέγα Μάθημα (Για την Επέτειο της 29ης Μαίου 1453

- Απαραίτητο Σημείωμα για τις 29 Μαίου

- Οι Δυο Πτώσεις της Πόλης και το Μέγα Μάθημα

- Στοχασμοί Ελληνικοί για την 29 Μαίου 1453

- Αμερικανική Ακμή και Ευρωπαική Παρακμή

- Medicophilosophica

- Ερευνα στην Γένεση και στις Αρχές της Ιπποκρατικής Σχολής

- Myth and Reality of Female to Male Transformation in Classical Antiquity

- An Extraordinary Birth in the Context of Similar Roman Prodigies: Macrosomia in a Hermaphroditic Newborn at Frusino, 207 BC

- Female to Male Sexual Transformation in Classical Antiquity

- A Hermaphroditic Newborn at Frusino, 207 B.C. in the Context of Similar Prodigies

- Απόλλων Επικούριος στις Βάσσες/Apollo Epicurius

- Πελασγικά Προλεγόμενα: Λύκαιον, Παρρασία, Βάσσαι

- Γη-Μήτηρ και Παν ο Μέγας

- Πελασγικά Πανικά Δρώμενα: Ιερατική Μαστίγωσις Διέγερσης

- "Παν ο Μέγας Τέθνηκεν" - Ιεροτελεστία του Έαρος: Συμβολισμοί Θανάτου και Ανάστασης σε Sumer και Αρκαδία

- Η Μέλαινα Δημήτηρ της Φιγαλείας: Φύση και Ιστορία της Λατρείας

- Δημήτηρ Ερινύς στην Θέλπουσα

- Προλεγόμενα σε Τιλφούσσα και Δελφούς: ο Ομηρικός Ύμνος εις Απόλλωνα

- Το Όνομα του Απόλλωνος

- Συμπεράσματα Επιγραμματικά Δεύτερης Επίσκεψης

- Λυκόσουρα, Λύκαιο και ο Ναός του Επικουρίου Απόλλωνος στις Βάσσες

- ΦΙΓΑΛΕΙΑΚΑ: Τόπος και Ιστορία, Θεοί και Πολιτισμός

- Αντί Επιλεγομένων της Γ' Συνάντησης: Εντοπισμός του Άντρου της Δήμητρος Μελαίνης στη Φιγαλεία

- Ο Ναός του Επικουρίου Απόλλωνος στις Βάσσες της Φιγαλείας. Το Αίνιγμα: Έρευνες και Προοπτικές, Ι

- Ο Ναός του Επικουρίου Απόλλωνος στις Βάσσες της Φιγαλείας. Το Αίνιγμα: Έρευνες και Προοπτικές, ΙΙ: Επιλεγόμενα

- Κριτικό Βιβλιογραφικό Σημείωμα

- Η Επιφάνεια του Δωρικού Απόλλωνα και η Ανάδυση της Μορφής του Κάλλους από τον Χθόνιο Κόλπο, την Ουράνια Βία και τον Τονικό Φαλλό

- Μορφολογικές Έρευνες - Classical Theory of Form

- Τραγικά - On tragedy

- Ολυμπιακές Μελέτες - Olympian Studies

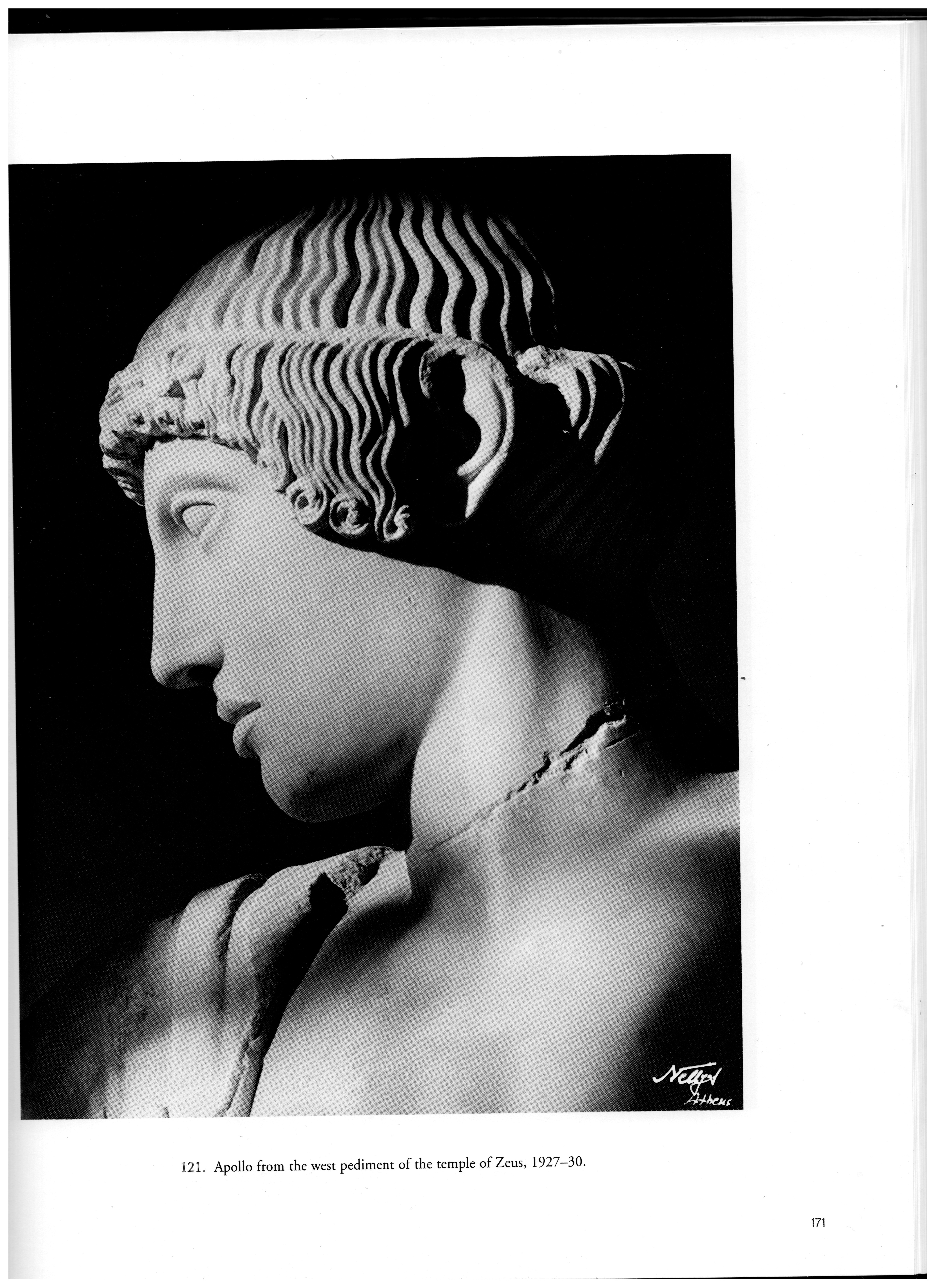

- Apollo (photo 1927 -30, Nelly's)

- Προλεγόμενα: Η Μεγάλη Μεταμόρφωση της Μορφής και ο Αττικός Δωρισμός

- Η Ανάδυση της Μορφής στα Ορειχάλκινα Ειδώλια της Ολυμπίας Ι.

- Η Ανάδυση της Μορφής στα Ορειχάλκινα Ειδώλια της Ολυμπίας ΙΙ.

- Η Ανάδυση της Μορφής στα Ορειχάλκινα Ειδώλια της Ολυμπίας ΙΙΙ.

- Η Μορφολογία του Δωρικού και του Ιωνικού Ρυθμού στην Πρώιμη Αρχαική Γλυπτική

- Το Δυτικό Αέτωμα του Ναού του Διός στην Ολυμπία: Έρευνες στην Αισθητή Ιδέα του Κλασσικού Ι - Ιστορικά, Χρονολογικά, Προκαταρκτικά

- Το Δυτικό Αέτωμα του Ναού του Διός στην Ολυμπία: Έρευνες στην Αισθητή Ιδέα του Κλασσικού ΙΙ - Η Αττική Προεργασία της Κλασσικής Μορφής

- Το Δυτικό Αέτωμα του Ναού του Διός στην Ολυμπία: Έρευνες στην Αισθητή Ιδέα του Κλασσικού ΙΙΙ - Δύο Πλαστικά Ρεύματα στην Πρώτη Γενεά της Αθηναικής Ελευθερίας - Αριστόδικος και Θησαυρός των Αθηναίων

- Το Δυτικό Αέτωμα του Ναού του Διός στην Ολυμπία: Έρευνες στην Αισθητή Ιδέα του Κλασσικού ΙV - Φειδίας, Αλκαμένης και ο ΑττικοΔωρικός Ρυθμός στην Πλαστική

- Έρευνες στην Δωρική Ουσία του Κλασσικού, Ι: Αγελάδας ο Αργείος και η Νέα Μορφή της Τελειότητας

- Ολυμπιακά Σεμινάρια, Ι: Ο Γλυπτικός Διάκοσμος του Ναού του Διός. Μορφολογική Ανάλυση και Υφολογική Ταυτοποίηση στα Πλαίσια των ρευμάτων Πλαστικής Αυστηρού Ρυθμού

- Ο Αλκαμένης και το Δυτικό Αέτωμα του Ναού του Διός στην Ολυμπία. Προβλήματα Μορφολογικής και Υφολογικής Ταυτότητας στο Πρώιμο Κλασσικό

- Η Χώρα του Αταίριαστου. Ολυμπιακά Αναθέματα

- Προβλήματα Δυισμού και ο Ελληνικός Μονισμός. Ο Συμβολισμός της Σχέσης των Φύλων

- Καίρια και Ουτιδανά για τους Ολυμπιακούς Αγώνες και την Ολυμπιακή Φλόγα

- Ολυμπιακοί Αγώνες: Γύμνωση και Αμεριμνησία

- Δωρικές Μελέτες - Dorian Studies

- Δωρικά Θεμέλια Μεταφυσικής, Θρησκείας, Πολιτισμού και Ιστορίας του Ελληνισμού

- Το Όνομα του Απόλλωνος: Έρευνα Γραμματικής Θρησκειολογίας του Ελληνισμού

- Το Νόημα των Κούρων

- Το Νόημα της Λυρικής Ποίησης

- Η Δωρική Μεταφυσική της Πολιτικής: Αριστεία και Μεγάλοι Αριθμοί στον Ελληνισμό και την Αθηναική Δημοκρατία

- Η Δωρική Δημιουργία: Πρωτοαρχαική Σπάρτη (Βασικά Κείμενα)

- Ευδαίμονες Ιεροβασίες: Σπάρτη

- Α' Χωρολογική Συνάντηση Σπάρτης

- Σπαρτιατικά

- Δαίδαλος, Δίποινος και Σκύλλις - η Πλαστική Μεταβάση από την Γεωμετρική στην Αρχαική Εποχή: Πηγές και Χρονολόγηση

- Δωρική και Ιωνική Υστερογεωμετρική και Πρωτοαρχαική Γλυπτική: Φιλολογική Έρευνα

- Η Ανάδυση της Μορφής στα Ορειχάλκινα Ειδώλια της Ολυμπίας Ι.

- Η Ανάδυση της Μορφής στα Ορειχάλκινα Ειδώλια της Ολυμπίας ΙΙ.

- Η Μορφολογία του Δωρικού και του Ιωνικού Ρυθμού στην Πρώιμη Αρχαική Γλυπτική Ι

- Η Ανάδυση της Μορφής στα Ορειχάλκινα Ειδώλια της Ολυμπίας ΙΙΙ.

- Η Μορφολογία του Δωρικού και του Ιωνικού Ρυθμού στην Πρώιμη Αρχαική Γλυπτική ΙΙ

- Κορινθιακή και Αττική Γλυπτική κατά τον 7ο και 6ο Αιώνα π.Χ.

- Βοιωτική Γλυπτική κατά τον 7ο και 6ο Αιώνα π.Χ.

- Μοίρα και Κάλλος: για μια Ελληνική Τελεολογική Μοιρολατρεία

- ΘΕΑΝΘΡΩΠΟΙ: Έρευνα στον Ελληνικό Θεομορφισμό

- Ο ΑΝΘΟΣ ΤΟΥ ΚΟΣΜΟΥ: Συμβολή στον Συμβολισμό της Φανέρωσης

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού Ι: Προκαθοδικές Έρευνες

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού ΙΙ: Το Ίνδαλμα του Κούρου

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού IΙΙ: Κρητικά Κουρητικά

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού IV: Από τον Κρητικό Μέγιστο Κούρο στον Δωρικό Απόλλωνα

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού V: Το Απολλώνιο Βίωμα του Κούρου. Δωριείς και Κουρήτες στην Στερεά Ελλάδα

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού VΙ: Κόρης, Κουρήτες και Διόσκουροι

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού VΙΙ: Οι Άβαντες του Κουρητικού Φωτός

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού VΙΙΙ: Λυκούργος - Δωρικός "Κόσμος" Πόλης, Ποίησης και Άθλησης

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού ΙX: Τα Πεπρωμένα της Σπάρτης στην Κοσμογονία του 8ου π.Χ. Αιώνα

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού Χ: Η Σπάρτη Οδηγός Ελληνισμού - Λακεδαιμόνιος Οργασμός στο Τέλος του 8ου π.Χ. Αιώνα

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού XI: Έρως Καλού - το Δωρικό Πνεύμα και η Δημιουργική Αρχή του Ελληνισμού

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού XII: Περί Δωρίδος, Α' ή Μορφή ως Τόπος

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού XIII: Περί Δωρίδος, Β' - ...Ερινεόν ηνεμόεντα. Το Πνεύμα των Ορέων, Οικήσεις και Μετοικήσεις, Μονές και Πρόοδοι

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού XIV: Το Αίνιγμα του Αρχαικού Χαμόγελου ή Τα Άνθη του Έαρος - το Μειδίαμα του Κούρου, το Παιχνίδι της Χαρμοσύνης και το Πνεύμα του Συμποσίου στην Σπάρτη

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού XV: Δελφική Αμφικτυονία

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού XVΙ: Οι Θυρεατικοί Στέφανοι και ο Απόλλων-Ζευς του Ugento

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού XVIΙ: Παιδός η βασιληίη - το Κοσμικό Παιχνίδι του Κάλλους

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού XVΙII: Ολυμπία, Ολύμπια Θρησκεία και η Μορφή του Απόλλωνα (Παράλληλοι Βίοι Ποίησης και Πλαστικής)

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού ΧΙΧ: Η Σοβαρή Παιδιά του Κάλλους - Απόλλων Γυμναστήριος και Φιλήσιος

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού ΧΧ: Η Δωρική Σπάρτη και η "Ώρα" του Ελληνισμού

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού ΧΧΙ: Έρως και Χρόνος - Ο Ανθός και ο Αδάμας της Σπάρτης

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού ΧΧΙΙ: Ο Κόσμος του Δαιμονικού ή το Κάλλος της Δύναμης (Θεοί, Άνθρωποι και Κοσμική Τάξη)

- Ο Χαρακτήρας της Δωρικής Ταυτότητας του Ελληνισμού ΧΧΙΙΙ: Το Δωρικό Πνεύμα και οι Πνοές του - Διεγέρσεις, Προσλήψεις, Αντιδράσεις (Πολιτσιμική Ιστορία του Ελληνισμού από τα Μέσα του 7ου στα Μέσα του 6ου Αιώνα π.Χ.) α

- Μορφολογία και Ύφος της Αρχαικής Λακωνικής Πλαστικής Ι. Ο Κούρος-Απόλλων του Κάλλους και της Ανδρείας (Ομάδα Αγαλματίων Α)

- Μορφολογία και Ύφος Αρχαικήσ Λακωνικής Πλαστικής, ΙΙ, Γυμνοπαιδιαί και οι ορειχάλκινοι "Θυρεατικοί" Παίδες (Ομάδα Αγαλματίων Β)

- Μορφολογία και Ύφος Αρχαικής Λακωνικής Πλαστικής, ΙΙΙ, Μορφές του Απόλλωνα σρην Σπάρτη: ο Οπλίτης του Απόλλωνα (Ομάδα Αγαλματίων Γ)

- Μορφολογία και Ύφος Αρχαικής Λακωνικής Πλαστικής, ΙV, Εξαπολλωνισμός του Δία: η Υπέρτατη Δύναμη του Κάλλους (ο Απολλώνιος Ζευς του Μονάχου)

- Έρευνες στην Δωρική Ουσία του Κλασσικού, Ι: Αγελάδας ο Αργείος και η Νέα Μορφή της Τελειότητας

- Στοχασμοί εξ Ικαρίας, Ι: Από Αριστερά Δεξιά ή από Δεξιά Αριστερά; Φορές Γραφής και Μεταφυσική των Κατευθύνσεων

- Reflections from Ikaria, II: Young Hercules and the Two Ways of Life

- Ενάτη Φθίνοντος Βοηδρομιώνος: η Εποπτεία των Μεγάλων Μυστηρίων και η Επιφάνεια του Άνακτα Υπερτελεάτα

- Έρευνες στον Σπαρτιατικό Τρόπο Βίου και την Βιοθεωρία του. Λακεδαίμων Εορτάζουσα Ι: Υακίνθια

- Έρευνες στον Σπαρτιατικό Τρόπο Βίου και την Βιοθεωρία του. Λακεδαίμων Εορτάζουσα ΙΙ: Γυμνοπαιδιαί

- Οι Μορφές του Απόλλωνος και οι Αξίες του Ελληνισμού

- Επίλογος στην Λακεδαιμόνια Εορταστική Εβδομάδα

- Πνοές από τις Λακεδαιμόνιες Γυμνοπαιδιές

- Κάρνεια Ιερομηνιακά

- Μη Ειωθυίες Επικαιρικές Ευχές: Περί θανάτου στον Χρόνο και Ζωής στην Αιωνιότητα - Δωρικές Πνοές

- Προλογικά εις Ορθίαν Άρτεμιν

- Εις Αναζήτηση της Ρίζας του Ελληνισμού: Δωδώνη και Πίνδος

- Περιοδοποίηση της Σπαρτιατικής Ιστορίας

- Εισαγωγικά Μεσσηνιακά

- Δελφική Πρόρρησις

- Ο Εξαπολλωνισμός της Θρησκευτικότητας στην Τέχνη του 7ου π.Χ. αι. και ο "Ανατολίζων " Ρυθμός

- Η Εμπλοκή: Αιωνιότητα και Χρόνος στην Αρχαική Σπάρτη

- Η Κρίση του 6ου αι. π.Χ.: Ο Δωρικός "Κόσμος" και η Ιωνική Προβολή

- Κάλλος και Χρόνος: Στοχασμοί πάνω στην Δόξα και την Μοίρα της Σπάρτης του 6ου αι. π.Χ.

- Το Είναι ως Ίστασθαι

- Απόλλων και Χρόνος: το Νόημα της Ιστορίας στον Χρυσούν Αιώνα

- Η Ομηρική "Μυκηναική" Λακεδαίμων: Όμηρος και Αρχαιολογία

- Υακίνθιοι Στοχασμοί

- Γυμνοί Στοχασμοί για τις Σπαρτιατικές Γυμνοπαιδιές: το Κάλλος και το Απόλυτο Νόημα της Ύπαρξης

- Ολυμπία και Σπάρτη: Ιδέα και Πραγματικότητα της Δωρικής Ουσίας του Ελληνισμού

- Περί του εν Δελφοίς Ε

- Το Θέατρο της Λακεδαίμονος: Φιλολογική και Αρχαιολογική Μελέτη Σπαρτιατικής Αλλοτρίωσης

- Το Αιώνιο Φως της Σπάρτης. - Στοχασμοί πάνω στην Ιδεώδη Ενότητα του Σπαρτιατικού Τρόπου

- Οι Δυο Όψεις του Αποκεκαλυμμένου και το Κεκρυμμένον

- Η Σπάρτη από το Θέρος στο Φθινόπωρο ή η Δωρική Πνοή στην Τάξη του Χρόνου

- Προς τον Έρωτα του Έαρος

- Έτος Λυκούργου

- Οι Εποχές της Σπαρτιατικής Ιστορίας

- Η Δωρική Μορφή και οι Προσλήψεις της στην Αρχαική Πλαστική

- Σπαρτιατικές Αρχές της Μορφολογίας και του Συμβολισμού του Κλασσικού: ο Αλκμάν και η Αρχή της Λυρικής Ποίησης, τα Λακωνικά και Διοσκουρικά Ανάγλυφα

- Γυμνοπαιδιές

- Απο-καλύψεις για τις Γυμνοπαιδιές

- Απόλλων Κεκρυμμένος: Η Ιδέα στον Χρόνο κατά την Εποχή της Παρακμής (Σπάρτη, Ελληνιστική Περίοδος και η Ρωμαική Λύση)

- Το Νόημα των Θερμοπυλών

- Σπάρτη, Αθήνα και ο Φειδιππίδης

- The Dorian Testament

- Η ΕΛΕΝΗ ΤΗΣ ΣΠΑΡΤΗΣ - Το Πνεύμα των Δωρικών Μεταμορφώσεων, Μέρος Α', Η Επική Παράδοση

- Η ΑΛΗΘΙΝΗ ΣΠΑΡΤΗ. Το Τρίπτυχο Ποιητικότητα - Αχρηματία - Ανομία

- Αφορισμοί στην Μεταφυσική του Κάλλους: Γιατί Υπάρχουν Χώρος, Χρόνος και Ιδέες;

- Η Αληθινή Σπάρτη

- Σπάρτη: το Είδωλο της Σκληρής Πειθαρχίας και η Ιδέα του Έρωτα του Κάλλους

- Sparta and Philosophy

- Για τα Κάρνεια, πάλι

- Για τις Θερμοπύλες

- Για τα Κάρνεια ακόμη μια φορά

- Αρχαία Ελληνική Ποίηση για την Σπάρτη. Εκλογή και Διόρθωση Αποσπασμάτων

- Διάκριση και Δια-κριτική (Σπαρτιατικά Ζητήματα με Αφορμή τον Εορτασμό των Θερμοπυλών)

- Τρόπος Ζωής Αρχαιοελληνικού Συμποσίου

- Η Δωρική Ιδέα και Θεμελιώδεις Δομές του Ελληνικού Τρόπου

- Φανερώσεις

- Απολλώνιες Μεταμορφώσεις

- Απόλλων και Δελφύνης

- Θεοφορικά Ποβλήματα. Η Δωρική πνοή και η Αντιπαλότητα Σπάρτης - Άργους

- Η Ώρα του Απόλλωνα. Αρχή και Τέλος. Γυμνοπαιδιές και Εκδυμάτια

- Ελληνισμός, Ευρώπη και η "καθ' ημάς" Ανατολή: Συγκριτικές Μελέτες Τριών Πολιτισμών

- Ελληνική Μορφή και Ευρωπαικό Σύστημα: η Περίπτωση των Αρχιτεκτονικών Ρυθμών στους δυο Πολιτισμούς

- Η Πολιτισμική Φύση του Χώρου και του Χρόνου

- Το Άγιν Είναι και ο Ρύπος του Γίγνεσθαι

- Τέλος και Αιών. Τελειότητα και Αιωνιότητα: οι δυο Όψεις μιας Ταυτότητας στον Κλασσικό και Βυζαντινορθόδοξο Ελληνισμό

- Η Περίοδος του Χρόνου και οι Εποχές των Πολιτισμών: Γέννα, Ακμή, Καρποφορία, Παρακμή και Θάνατος

- Αυτοσχέδιες Σκέψεις για την Ταυτότητα και Συνέχεια του Ελληνισμού και για το Ευρωπαικό Ζήτημα

- Ανατολική Μεσόγειος και το Κεντρικό Σύστημα της Ιστορίας

- Θανάσιμα και Αναστάσιμα

- Το Κεντρικό Σύστημα της Ιστορίας, 2η έκδοση - Ο Θάνατος της Ευρώπης και η Ανανέωση του Κόσμου

- Οντολογικές Ευχές

- Απόστολος Αθανασίας

- Στο Μουσείο της Σπάρτης

- Φαινόμενα του Σπαρτιατικού Θαύματος. ΚΟΡΟΙ, ΙΠΠΑΓΡΕΤΑΙ, ΑΓΑΘΟΕΡΓΟΙ: από το Κάλλος στο Αγαθό. Το Ανάγλυφο του Θιοκλή

- Μια Ομάδα Αρχαικών Λακωνικών Αναγλύφων. Οι Διόσκουροι της Σπάρτης: μια Μεταμόρφωση

- Τα Ανάγλυφα των Χθονίων Θεοτήτων (Άδης-Διόνυσος και Περσεφόνη-Αφροδίτη) Α'

- Ο Αθλητικός Αρύβαλλος του Πολυδεύκη, η Διακοσμητική Παράδοση στον Βαθυκλή, και ο Συμβολισμός του Ροδιού

- Η Αλλαγή Φοράς στα Χθόνια Λακωνικά Ανάγλυφα και η Τροπή της Σπάρτης κατά τα Μέσα του 6ου π.Χ. Αιώνα

- Κοινά ΜΟεφολογικά και Συμβολικά Στοιχεία μςταξύ των Χθονίων Λακωνικών Αναγλύφων και της Μεσοποταμιακής Μυθολογίας και Εικονογραφίας

- Μεγαρικά

- Νεοελληνισμός

- Ανεπηρέαστες Σκέψεις για το 1776 και το 1821

- Η Επανάσταση του 1821. Πνεύμα και Ιστορία, Νόημα και Γεγονότα

- Αρχαία και Νέα Σπάρτη

- Ελεύθεροι Στοχασμοί επί της Νεοελληνικής Πραγματικότητας

- Η Κακοδαιμονία: Συνέπειες μιας Αλλοτρίωσης. Ευχετήριοι Διαλογισμοί

- Τί Δεν Φταίει

- Απλές Φιλοσοφικοιστορικές Σκέψεις για ένα νέο Ελληνικό Στρατηγικό Δόγμα

- Ανθεστήρια και Καρνάβαλος (Το Αρχέτυπο και η Καρικατούρα)

- Σημάδια και Σημασίες

- Σημείωμα Β' περί Κορονοιού, βραχύ

- Ελληνισμός και Νεοελληνισμός: Μια Αντίθεση

- Οι Θεοί του Ελληνισμού, τα Είδωλα της Ευρώπης και η Πονηρία του Νεοελληνικού Συστήματος

- Περί Ιού, Υστερίας, Αξιοπρέπειας και Κλασσικού

- Λακωνικά περί Ορθής Πολιτείας και Ορθ'ωσεως Εσφαλμένης

- Αλλοτρίωση και Κλεψικρατία

- Τί Φταίει;

- Τί Φταίει; Β΄ Έκδοση

- nascenti puero

- Κάλλος και Ιστορία. Ο Δωρικός Άξονας

- Αυτοκρατορία και Ελληνική Πόλη: Ashurnarsipal II και Λυκούργος

- Σπάρτη και Αυτοκρατορία στο Μέσον του 6ου αι. π. Χ.

- Σπάρτη και Περσική Αυτοκρατορία. Δόγμα Δυο Ζωνών Επιρροής, 3ο τέταρτο 6ου αι. π. Χ.

- Η Επανάσταση του Άνθους: Υάκινθος

- Η Επανάσταση του Άνθους: ο "Λακωνικός Ιππεύς"

- Η Επιφάνεια του Δωρικού Απόλλωνα και η Ανάδυση της Μορφής του Κάλλους από τον Χθόνιο Κόλπο, την Ουράνια Βία και τον Τονικό Φαλλό

- Η Δωρική Ιδέα και Θεμελιώδεις Δομές του Ελληνικού Τρόπου

- Θεοφορικά Ποβλήματα. Η Δωρική πνοή και η Αντιπαλότητα Σπάρτης - Άργους

- Η Ώρα του Απόλλωνα. Αρχή και Τέλος. Γυμνοπαιδιές και Εκδυμάτια

- Σπάρτη και Ολυμπία

- Δογματικά Ελληνισμού

- Ο Απόλλων και το Αίνιγμα του Χρόνου

- Αφορισμοί Πνευματικών 'Αρθρων

- Απόλλων και Χριστός

- Πολιτισμοί. Στοχασμοί πάνω στο Κλασσικό, το Βυζαντινό και το Ευρωπαικό

- Μεταφυσική Δογματική του Ελληνισμού

- Οντολογικές Αρχές Ιστορίας του Πολιτισμού

- Η Δωρική Ιδέα και Θεμελιώδεις Δομές του Ελληνικού Τρόπου

- Θανάσιμα και Αναστάσιμα

- Η Πνοή του Κάλλους Πνεύμα Θεού

- Φανερώσεις

- Απολλώνιες Μεταμορφώσεις

- Απόλλων και Δελφύνης

- Κάλλος και Ελληνισμός

- Αμεριμναίοι. Η παιδιά της Αιωνιότητας στον Χρόνο

- Προβλήματα Δυισμού και ο Ελληνικός Μονισμός. Ο Συμβολισμός της Σχέσης των Φύλων

- Η Αιωνιότητα του "Τέλους"

- Η Μορφή της Ιστορίας και η Κατάσταση του Κόσμου

- Video links

- 200ετηρίς Επαναστάσεως - Προβλήματα Νεοελληνισμού

- Τα Αταίριαστα. - Δυσαρμονίες Ταυτότητας

- Α¨. Και πάλι ο Φειδιππίδης, φευ!

- B: Ολυμπία και Τεχνολογία: η απόλυτη Αντίφαση

- Γ¨ Η Μεγάλη Πτώση της Μεγάλης Εκκλησίας: Υποταγή στην Κοσμική Εξουσία και Ιδεολογία της Ένωσης

- Δ' Η Ακρόπολη και το Άμουσο Μουσείο της: το Θαύμα και το Σύμπλεγμα

- Ε' Το Θέατρο της Λακεδαίμονος. Φιλολογική και Αρχαιολογική Μελέτη Σπαρτιατικής Αλλοτρίωσης

- ΣΤ΄ Τα Αγάλματα του Άργους. Η Μεγάλη Αργεία Πλαστική Παράδοση και η Σύγχρονη Ύβρη

- Αταίριαστα Ζ, Η Χώρα του Αταίριαστου. Ολυμπιακά Αναθέματα

- Αταίριαστα Η, Τα Αγάλματα του Άργους Β, Η Μανία του Αταίριαστου ή ο Απόλλων και η Ήρα

- Για την Σπάρτη της Αλλοτρίωσης

- Λυκούργος, Μαντείο των Δελφών και Delacroix

- Σπαρτιάτης

- Value, Money And Credit In Ancient Greek Market Economy

- Seminars

- Εισαγωγικά και Γενικά

- ΚΑ' Κύκλος

- ΚΒ Κύκλος

- Κύκλος ΚΒ΄ Α

- Κύκλος ΚΒ΄ B

- Σεμινάρια ΚΓ

- Κύκλος ΚΔ'

- Παράπλευρες Εκδηλώσεις

- 2ο Αρχαιοελληνικό Συμπόσιο

- 2ο Αρχαιοελληνικό Συμπόσιο Ισημερίας

- Συμπόσιο της Ισημερίας - Αντίνοος

- Συμπόσιο της Ισημερίας - Προβολές

- Συμπόσιο της Ισημερίας - Απόψεις και Συντελεστές

- Συμπόσιο της Ισημερίας - Συντονισμοί

- Δ' ΑρχαιοΕλληνικό Συμπόσιο

- Αρχαία Συμπόσια

- Γ' Αρχαιοελληνικό Συμπόσιο

- Ε΄ Αρχαιοελληνικό Συμπόσιο

- Περί Χειμερινών Τροπών, Ηλιολογίας και Ηλιολατρείας, Φαλλικών Αττικών Εορτών και Μεγάλων Συνόδων Πλανητών

- ΣΤ' ΑρχαιοΕλληνικό Συμπόσιο - Περί Εαρινής Ισημερίας και Έρωτος

- Ζ' Αρχαιοελληνικό Συμπόσιο

- Η' ΑρχαιοΕλληνικό Συμπόσιο

- Θ' ΑρχαιοΕλληνικό Συμπόσιο, Θερινό Ηλιοστάσιο 2013

- Ι' ΑρχαιοΕλληνικό Συμπόσιο - Χειμερινές Τροπές 2013

- ΙΑ' ΑρχαιοΕλληνικό Συμπόσιο - Εαρινή Ισημερία 2014

- Συμπόσιο Ανθεστηρίων

- ΑρχαιοΕλληνικό Συμπόσιο για τις Χειμερινές Τροπές 21 Δεκεμβρίου 2016

- Κύκλος ΚΕ'

- Πρόγραμμα 2011 - 2012

- Η Ουσία του Ανθρώπου: ο Λόγος και όχι το Υποκείμενο Εγώ

- Ισορροπία Δυνάμεων στο Τέλος της 2ης Χιλιετίας π.Χ.

- Ολοκλήρωση Γεωπολιτικών Χώρων και Λόγος

- Ο Λόγος και η Εποχή του Σιδήρου: το Ελληνικό Φαινόμενο

- Η Σύλληψη της Επανάστασης του Λόγου: οι Σκοτεινοί Αιώνες

- Οι Κάθοδος των Δωριέων, το Έπος και οι Ολυμπιακοί Αγώνες

- Ο Απόλλων και οι Δωριείς

- Οι Δωριείσ και οι Έλληνες: η Γένεση του Ελληνισμού

- Οι Μεταρρυθμίσεις του Σόλωνος και η Εθνική Προδοσία Σήμερα

- Ευρωπαική Τεχνητότητα και το Καθεστώς των Γραικύλων

- Σεμινάριο 12 + Λαικισμός στην Κλασσική Αθήνα

- Σεμινάριο 13 + Ελληνικό Πνεύμα και Ευρωπαικό Αντι-πνεύμα

- Σεμινάριο 21ο + Η Αιτία του Εγκλήματος Καθοσιώσεως του Καθεστώτος κατά της Ελλάδας: Ευρωπαισμός

- Σεμινάριο 14 + Η Προδοσία του Καυεστώτος της Φαυλοκρατίας και το Μωρογέλοιον του Ευρωπαισμού τώρα και της Ένωσης τότε

- Σεμινάριο 15 + Άνοιξη - Ευαγγελισμός - Επανάσταση. Το νόημα του Τριπλου Συμβόλου και η Τριπλή Προδοσία του ΝεοΕλληνισμού

- Σεμινάριο 16 + Ο Θρίαμβος του Πνεύματος

- Σεμινάριο 17 + Το Θαύμα και η Τραγωδία της Αθήνας + περί Περικλή Γιαννόπουλου

- Σεμινάριο 18 + Οι Εκλογές της Απάτης

- Σεμινάριο 19 + ΑΠΟΧΗ!

- Σεμινάριο 20 + Θρίαμβος

- Σεμινάριο 21ο + Η Αιτία του Εγκλήματος Καθοσιώσεως του Καθεστώτος κατά της Ελλάδας: Ευρωπαισμός

- Σεμινάριο 22 + Στοιχείωσις Οντολογική τησ Απόλυτης Αντίφασης Ελληνισμού και Ευρωπαισμού

- Σεμινάριο 23 + ΤΙ ΣΥΜΒΑΙΝΕΙ; Ο Βαρβαρισμός του 20ου αιώνα και η Αυγή του 21ου

- Σεμινάριο 24 + Ελλάδα και Ευρώπη

- Σεμινάριο 27 + Τρία Κείμενα Αποτροπιασμού, Θλιμένης Σκέψης και Χαρούμενης Γνώσης

- Σεμινάριο 26 + Οι Ληστρικές Εκλογές της !7ης Ιουνίου

- Σεμινάριο 28 + Η Αρχή του Όντος + Η Κατάρρευση της Ευρώπης

- Σεμινάριο 29 + Χρονολόγιο + Ύδατα Στυγός

- Σεμινάριο 30 + Ο Ηρακλείτειος Κόσμος

- Διάφορα Σεμινάρια

- Η Τεχνική της Πρόβλεψης, η Λογική της Ανάπτυξης και η Αρχαία Ελληνική Σκέψη

- Το Αγωνιστικό Ιδεώδες της Ζωής στην Κλασσική Αρχαιότητα και η Σημασία του στην Σύγχρονη Πραγματικότητα

- Το Χρήμα και η Πραγματική Οικονομία στην Ιστορία και στον 21ο Αιώνα

- Πολιτική και Οικονομία στον 21ο Αιώνα

- Ελληνισμός, Ευρωπαικόσ Πολιτισμός και Ιστορία

- Η Ιδεολογία της Αριστείας σε έναν Πολιτισμό της Επιτυχίας

- Ο Κύκλος και ο Σκοπός της Ιστορίας

- Ιδεολογία της Ανακαινίσεως και Ανακαίνισις της Ιδεολογίας

- Φιλοσοφία, Θρησκεία και Πολιτική στην Μεγάλη Ελλάδα: το Πυθαγόρειο Κίνημα

- Κύκλος ΚΣΤ'

- Πρόγραμμα Περιόδου 2012-3

- 1ο Σεμινάριο

- 2ο Σεμινάριο

- 3ο Σεμινάριο

- 4ο Σεμινάριο

- 5ο Σεμινάριο

- 6ο Σεμινάριο

- 7ο Σεμινάριο

- 9ο Σεμινάριο

- Σεμινάριο 10ο

- Σεμινάριο 11ο

- Σεμινάριο 12ο

- Σεμινάριο 13ο

- Σεμινάριο 14ο

- Σεμινάριο 15ο

- Σεμινάριο 16ο

- Σεμινάριο 17ο

- Σεμινάριο 18ο

- Σεμινάριο 19ο

- Σεμινάριο 20ο

- Εκδηλώσεις Εβδομάδας 13-20 Μαίου 2013

- Συνέχεια Εκδηλώσεων Εβδομάδας 13-20 Μαίου 2013

- Σεμινάριο 22ο

- Σεμινάριο 23ο

- Σεμινάριο 24ο

- Σεμινάριο 25ο

- Σεμινάριο 26ο

- Σεμινάριο 27ο

- Σεμινάριο 28ο

- Σεμινάριο 29ο

- Σεμινάριο 30ο

- Καλλιτεχνικά Προγράμματα

- Βοιωτικά

- Το Πρόβλημα του Νεοελληνισμού ειναι ο Ίδιος ο Νεοελληνισμός

- Συνέντευξη

- Προς τους Έλληνες

- Το Νέο Leviathan

- Η Τρίτη Επανάσταση

- Που Βρίσκεται η Αρρώστεια;

- Τί Θέλει το Σύστημα και Γιατί

- Τέρμα τα Ψέμματα και Τέλος Εποχής

- Η Παγκόσμια Οικονομική Κρίση και η Κρίση της "Ευρώπης"

- Η Υψηλή Στρατηγική των ΗΠΑ

- Το Οικονομικό Πρόβλημα των ΗΠΑ

- Φιλοσοφική Πολιτική για μια Αποτυχημένη Χώρα

- Φιλοσοφική Ανάλυση για μια Αποτυχημένη Χώρα

- Όροι για μια Επιτυχή Στρατηγική Ανάταξης

- Πολιτειακή Αναδόμηση: το Μεικτό Σύστημα

- Η Εξέλιξη του Συσχετισμού Ισχύος στο Παγκόσμιο Σύστημα τον 20ο Αιώνα

- Στρατηγική Αναγέννησης: Πολιτειακή Δομή

- Εξωτερική Πολιτική

- Το Τέλος της Νεοελληνικής Φαυλοκρατίας και η Αρχή του Τέλους της Ευρωζώνης

- Η Φαυλοκρατία και ο "Ξένος Παράγοντας"

- Ο Θάνατος της "Ευρώπης": η Συντριβή του Τεχνητού από το Φυσικό

- Η Προδοσία του Καθεστώτος της Φαυλοκρατίας και το Μωρογέλοιον του Ευρωπαισμού Τώρα και της Ένωσης Τότε

- Ελλάδα και Ευρώπη: το Ολικό Σύνθετο Ασύμβατο και οι Εκλογές του 2012

- Οι Εκλογές της Απάτης

- ΑΠΟΧΗ!

- Θρίαμβος! Η Ανυπέρβλητη Φρόνηση των Μεγάλων Αριθμών

- Ευρωπαισμός

- Στοιχείωσις Οντολογική της Απόλυτης Αντίφασης Ελληνισμού και Ευρωπαισμού

- Τί Συμβαίνει; Ο Βαρβαρισμός του 20ου Αιώνα και η Αυγή του 21ου

- Ελλάδα και Ευρώπη

- Η Σημασία των Εκλογών της 17ης Ιουνίου 2012

- Οι Ληστρικές Εκλογές της 17ης Ιουνίου 2012

- Η Εσωτερική Αηδία - Γερμανία και Ευρώπη - Το Τέλος της Βαρβαρικής Εποχής

- Η Αρχή του Όντος - Η Κατάρρευση της Ευρώπης

- Ατιμωτική Συνεύρεση

- Ελληνικό Μάθημα προσ την Καγκελλάριο της Γερμανίας

- ΟΧΙ!

- Bulgaria's Lesson on Euro-Madness

- Κύκλος ΚΣΤ' Παράλληλη Σειρά

- Προκαταρκτικό πρόγραμμα

- Σεμινάριο 2ο

- Σεμινάριο 5ο

- Σεμινάριο 6ο

- Πρώιμος Επικός Κύκλος

- Σεμινάριο 7ο. - Η Δωρική Δημιουργία: Πρωτοαρχαική Σπάρτη

- Σεμινάριο 8ο. - Άγιο και Βέβηλο, Εσθλό και Δειλό στην Αρχαική Εποχή

- Σεμινάριο 9ο. - Αρχίλοχος και Στησίχορος: οι δύο Πόλοι του Λυρισμού

- Σεμινάριο 10ο

- Το Θήλυ στον Πολιτισμό του Κάλλους

- Σεμινάριο 11ο

- Έρως και Έαρ Ήρωος Άρρενος

- Σεμινάριο 12ο

- Η Απόλυτη Κλήση της Τελειότητας

- Ελληνισμός, Γερμανισμός της Ευρώπης και το Αισχρό Καθεστώς του ΝεοΕλληνικού Ψευδοκράτους

- Ελλάδα, Γερμανία, Ευρώπη

- Η Αθλιότητα του ΝεοΕλληνικού Καθεστώτος και το Κέντρο του Κόσμου

- Και πάλι περί Ελλάδας, Γερμανίας και Ευρώπης

- Η Αθλιότητα του Νυν και το Αιώνιο Μεγαλείο του Ελληνισμού

- Το νέο Κυπριακό Πρόβλημα, το Αίσχος του Καθεστώτος και η Αθήνα του Πελοπονννησιακού Πολέμου

- Η Μοίρα της Ευρώπης και η Αισχρότητα των Πιθήκων

- Ο Αδήριτος Νόμος της Ομοιότητας: Ελληνισμός και η Καταισχύνη του Καθεστώτος της Χώρας

- Ελληνισμός και Γερμανισμός

- Ελληνισμός και Ελληνική Ηθική

- Χρόνος, Αιωνιότητα και Επικαιρικοί Αφορισμοί

- Το Επαίσχυντο Καθεστώς του ΝεοΕλληνισμού: Ο Πίθηκος

- Κύκλος ΚΖ'

- Αναγγελτήριο

- Πρόγραμμα

- Σεμιναριο 1ο

- Σεμινάριο 2ο

- Σεμινάριο 3ο

- Σεμινάριο 4ο

- Σεμινάριο 5ο

- Σεμινάριο 6ο

- Σεμινάριο 7ο

- Σεμινάριο 8ο

- Σεμινάριο 9ο

- Σεμινάριο 10ο

- Σεμινάριο 11ο

- Σεμινάριο 12ο

- Σεμινάριο 13ο

- Σεμινάριο 14ο

- Σεμινάριο 15ο

- Σεμινάριο 16ο

- Σεμινάριο 17ο

- Σεμινάριο 18ο

- Σεμινάριο 19ο

- Σεμινάριο 20ο

- Σεμινάριο 21ο

- Σεμινάριο 22ο

- Σεμινάρια 23ο και 24ο

- Σεμινάριο 24ο

- Σεμινάριο 25ο

- Σεμινάριο 26ο

- Σεμινάρια τελευταία

- Σεμινάρια τέλους

- Σεμινάρια 28ο και 29ο

- Σεμινάριο Έκτακτο

- Επιστολή προς την Καγκελλάριο της Γερμανίας - Letter to the German Chancellor

- Επικαιρικά Κείμενα

- Χωρολογικές Συναντήσεις

- Α' Χωρολογική Συνάντηση: Λυκαία

- Β' Χωρολογική Εκδρομή: Αττική Επακρία και Διακρία

- Γ' Χωρολογική Συνάντηση: Λυκαία - Βάσσες

- Δ' Χωρολογική Συνάντηση: Αργολίδα

- Ε΄ Χωρολογική Συνάντηση: Ολυμπία

- ΣΤ΄ Χωρολογική Συνάντηση: Σπάρτη (Α΄ Περιόδου 2014 - 2015)

- Ζ' Χωρολογική Συνάντηση Θέρμος (Β' Περιόδου 2014-2015)

- Η' Χωρολογική Συνάντηση Θήβαι-Βοιωτία (Γ' Περιόδου 2014-2015)

- Θ' Χωρολογική Συνάντηση Στεμνίτσας (Δ' Περιόδου 2014-2015)

- Θ' Χωρολογική Συνάντηση Στεμνίτσας (Δ' Περιόδου 2014-2015) - ΙΙ

- Ι' Χωρολογική Συνάντηση - Αργολίς (Ε' Περιόδου 2014-2015)

- ΙΑ' Χωρολογική Συνάντηση: Ολυμπία (ΣΤ' Περιόδου 2014-2015)

- ΙΒ' Χωρολογική Συνάντηση: Φιγάλεια (Ζ' Περιόδου 2014-2015)

- ΙΓ' Χωρολογική Συνάντηση: Μονεμβασία (Η' Περιόδου 2014-2015)

- Α' Χωρολογική Συνάντηση Περιόδου 2015-2016: Δωρίς, 4-6 Μαρτίου 2016

- Β' Χωρολογική Συνάντηση Περιόδου 2015-2016: Σπάρτη και Ταύγετος, 17-21 Ιουνίου 2016

- Βραχύς Απόλογος για την Χωρολογική Συνάντηση και ΑρχαιοΕλληνικό Συμπόιο: Σπάρτη και Ταύγετος

- Γ' Χωρολογική Συνάντηση Περιόδου 2015-2016: Συνάντηση της Ανδρίτσαινας - Ναός του Επικουρίου Απόλλωνος και Φιγαλεία, 29 Ιουλίου - 2 Αυγούστου 2016

- Μεταξύ Περιόδων Ι (Αύγουστος 2016)

- Μεταξύ Περιόδων ΙΙ: Στυξ, Χωρολογική Συνάντηση της Ζαρούχλας (26-28 Αυγούστου 2016)

- Μεταξύ Περιόδων ΙΙΙ: ΑΝΑΒΟΛΗ! Οι Περιπέτειες του Προφανούς στους Θυρωρούς των Ανακτόρων του Μηδενός

- Μεταξύ Περιόδων ΙV: Αρχαιοελληνικό Συμπόσιο για την Φθινοπωρινή Ισημερία (22 Σεπτεμβρίου 2016)

- Κύκλος ΚΗ΄

- Πρόγραμμα Περιόδου 2014 - 2015

- Σεμινάριο 1ο

- Σεμινάριο 2ο

- Σεμινάριο 3ο

- Σεμινάριο 4ο

- Σεμινάριο 5ο

- Σεμινάριο 6ο

- Σεμινάριο 7ο

- Σεμινάριο 8ο

- Σεμινάριο 9ο

- Σεμινάριο 10ο

- Σεμινάριο 11ο

- Σεμινάριο 12ο

- Σεμινάριο 13ο

- Σεμινάριο 14ο

- Σεμινάριο 15ο

- Σεμινάριο 16ο

- Σεμινάριο 17ο

- Σεμινάριο 18ο

- Σεμινάριο 20ο

- Σεμινάριο 21ο

- Σεμινάριο 22ο

- Σεμινάριο 23ο

- Σεμινάριο 24ο

- Σεμινάριο 25ο

- Σεμινάριο 26ο

- Σεμινάριο 27ο

- Σεμινάριο 28ο

- Σεμινάριο 29ο

- Σεμινάριο 30ο

- Σεμινάριο 31ο

- Σεμινάριο 32ο

- 1ο Συμπληρωματικό Σεμινάριο

- 2ο Συμπληρωματικό Σεμινάριο

- 3ο Συμπληρωματικό Σεμινάριο

- Μανιφέστο και Εκδηλώσεις Σεπτεμβρίου

- Κύκλος ΚΘ'

- Σεμινάριο 1ο

- Σεμινάριο 2ο

- Σεμινάριο 3ο

- Πρόγραμμα Σεμιναρίων περιόδου 2015 - 2016

- Σεμινάριο 4ο

- Σεμινάριο 5ο

- Σεμινάριο 6ο

- Σεμινάριο 7ο

- Σεμινάριο 8ο

- Σεμινάριο 9ο

- Σεμινάριο 10ο

- Σεμινάριο 11ο

- Σεμινάριο 12ο

- Σεμινάριο 13ο

- Σεμινάριο 14ο

- Σεμινάριο 15ο

- Σεμινάριο 16ο

- Σεμινάριο 17ο

- Σεμινάριο 18ο

- Σεμινάριο 19ο

- Σεμινάριο 20ο

- Σεμινάριο 21ο

- Σεμινάριο 22ο

- Σεμινάριο 23ο

- Σεμινάριο 24ο

- Σεμινάριο 25ο

- Σεμινάριο 26ο

- Σεμινάριο 27ο

- Σεμινάριο 28ο

- Σεμινάριο 29ο

- Σεμινάριο 30ο

- Σεμινάριο 31ο

- Σεμινάριο 32ο

- Σεμινάριο 33ο: "Τέλος" φετινής Περιόδου - Καταληκτικό Σεμινάριο και Χωρολογική Συνάντηση

- Κύκλος Λ', Συναντήσεις Πατρών και Σπάρτης

- Πρόγραμμα Σεμιναρίων Πατρών

- Πρόγραμμα Σεμιναρίων Σπάρτης

- Σεμινάριο 1ο Πατρών και 1ο Σπάρτης

- Σεμινάριο 2ο Πατρών

- Σεμινάρια 3ο πατρών, 2ο Σπάρτης και Ομιλία στην Αρχαία Ολυμπία

- Σεμινάριο 4ο Πατρών

- Σεμινάριο 5ο Πατρών και 3ο Σπάρτης

- Σεμινάριο 6ο Πατρών και 4ο Σπάρτης

- Σεμινάριο 7ο Πατρών

- Σεμινάριο 8ο Πατρών και 5ο Σπάρτης

- Σεμινάριο 9ο Πατρών

- Σεμινάριο 10ο Πατρών και 6ο Σπάρτης

- Σεμινάριο 11ο Πατρών και 7ο Σπάρτης

- Σεμινάριο 12ο Πατρών

- Σεμινάριο 13ο Πατρών και 8ο Σπάρτης

- Σεμινάριο 14ο Πατρών

- Σεμινάριο 15ο Πατρών και 9ο Σπάρτης

- Σεμινάριο 16ο Πατρών

- Σεμινάριο 17ο Πατρών και 10ο Σπάρτης

- Σεμινάριο 18ο Πατρών

- Σεμινάριο 11ο Σπάρτης

- Σεμινάριο 12ο Σπάρτης

- Σεμινάριο 19ο Πατρών

- Σεμινάριο 20ο Πατρών

- Σεμινάριο 14ο Σπάρτης

- Σεμινάριο 21ο Πατρών

- Σεμινάριο 22ο Πατρών, Ομιλία στην Κυπαρισσία και Λακεδαιμόνια Εβδομάδα

- Λακεδαιμόνια Εβδομάδα

- Χωρολογικές και Αρχαιολογικές Έρευνες και Συναντήσεις Θέρος 2017, Ι: Ιούλιος

- Σεμινάριο 24ο Πατρών

- Σεμινάριο 25ο Πατρών

- Σεμινάριο 26ο Πατρών

- Για τις Γυμνοπαιδιές

- Συμπόσιο για τις Γυμνοπαιδιές

- Σεμινάριο 27ο Πατρών

- Χωρολογικές και Αρχαιολογικές Έρευνες και Συναντήσεις Θέρος 2017, ΙΙ: Αύγουστος

- Για τα Κάρνεια

- Χωρολογικές και Αρχαιολογικές Έρευνες και Συναντήσεις Θέρος 2017, ΙΙΙ: Σεπτέμβριος

- Σεμινάριο 13ο Σπάρτης

- Σεμινάριο 23ο Πατρών

- Σεμινάρια 4ο Πατρών, 3ο Σπάρτης και Ομιλία στην Αρχαία Ολυμπία

- Συναντήσεις Πατρών ΛΑ' και Σπάρτης Β'

- Συναντήσεις Πατρών ΛΑ' Κύκλος - Πρόγραμμα

- Συναντήσεις Σπάρτης Β'' Κύκλος - Πρόγραμμα

- 4η Εκδήλωση Μεσοπεριόδου και Αναγγελία Β' Κύκλου (2-5 Νοεμβρίου 2017)

- Σεμινάριο 1ο Πατρών και 1ο Σπάρτης

- Σεμινάριο 2ο Πατρών

- Σεμινάρια 3ο Πατρών και 2ο Σπάρτης

- Σεμινάρια 5ο Πατρών και 3ο Σπάρτης

- Σεμινάριο 6ο Πατρών και 4ο Σπάρτης

- Σεμινάριο 7ο Πατρών

- Σεμινάριο 8ο Πατρών και 5ο Σπάρτης

- Σεμινάριο 9ο Πατρών

- Σεμινάριο 10ο Πατρών

- Σεμινάριο 11ο Πατρών και 7ο Σπάρτης

- Σεμινάριο 12ο Πατρών

- Σεμινάριο 13ο Πατρών και 8ο Σπάρτης

- Σεμινάριο 14ο Πατρών

- Συμπόσιο Εαρινής Ισημερίας, Σεμινάριο 15ο Πατρών και 9ο Σπάρτης, Εκδήλωση στην Σπάρτη για το 21 και τον Ευαγγελισμό, Ειδική Εκδήλωση στην Ολυμπία για τα Γλυπτά του Ναού του Διός

- Σεμινάριο 16ο Πατρών και 9ο Σπάρτης

- Σεμινάριο 17ο Πατρών και Χωρολογική και Αρχαιολογική Συνάντηση Ελευσίνας

- Σεμινάριο 18ο Πατρών και 11ο Σπάρτης

- Σεμινάριο 19ο Πατρών και Συναντήσεις Τέχνης 1η

- Σεμινάριο 20ο Πατρών και 12ο Σπάρτης

- Σεμινάριο 21ο Πατρών Και Συναντήσεις Τέχνης 2η

- Συναντήσεις Τέχνης 3η, Σεμινάριο 24ο Πατρών και 14ο Σπάρτης

- Σεμινάριο 25ο Πατρών

- Συναντήσεις Τέχνης 4η, Συμπόσιο Θερινών Τροπών, Ομιλία στα Σπαντίδεια Υακίνθια και Ομιλία στο Ξηροκάμπι

- Σεμινάριο 26ο Πατρών και Συναντήσεις Τέχνης 5η

- Συναντήσεις Τέχνης 5η, Σεμινάριο 27ο Πατρών και Συνάντηση Αργολίδας

- Σεμινάριο 28ο Πατρών και Υακίνθια Σπάρτης

- Συναντήσεις Τέχνης 6η, Σεμινάριο 29ο Πατρών

- Σεμινάριο 30ο Πατρών και Καταληκτικό Συμπόσιο στην Έκλσιψη Σελήνης

- Σεμινάρια 22ο και 23ο Πατρών, 13ο Σπάρτης, Ειδικές Εκδηλώσεις στην Σπάρτη και στην Κάτω Αχαία

- Συναντήσεις Σπάρτης Μεσοπεριόδου 2η

- Εκδηλώσεις Μεσοπεριόδου Θέρους-Φθινοπώρου 2017

- Παράπλευρες Ειδικές Εκδηλώσεις 2018

- Δυο Ομιλίες στο Ληξούρι

- Ομιλία στα Σπαντίδεια Υακίνθια

- Συμπόσιο για τις Θερινές Τροπές 2018

- Χωρολογικές και Αρχαιολογικές Έρευνες και Συναμτήσεις: Αργολίδα

- Υακίνθια 2018 Σπάρτη: Τριπλή Εορτή Λόγου και Αισθήσεων

- Ειδική Εκδήλωση στην Κάτω Αχαία για την Κατάσταση στην Χώρα

- Δυο Εκδηλώσεις στην Σπάρτη για τις Γυμνοπαιδιές

- Δυο Εκδηλώσεις στην Σπάρτη για τα Κάρνεια 2018

- Ειδική Εκδήλωση στην Σπάρτη για την Επέτειο της Πτώσηςτης Πόλης

- Εκδηλώσεις για την Φθινοπωρινή Εορτή της Ορθίας Αρτέμιδος

- Συναντήσεις Πατρών ΛΒ' και Σπάρτης Γ'

- Συναντήσεις Πατρών Κύκλος 32ος Α' Μέρος

- Συναντήσεις Πατρών Κύκλος 32ος Β' Μέρος

- Συναντήσεις Πατρών Κύκλος 32ος Γ' Μέρος

- Συναντήσεις Πατρών Κύκλος 32ος Δ' Μέρος

- Συναντήσεις Σπάρτης Κύκλος Γ'

- Συναντήσεις Σπάρτης Εισαγωγική Εκδήλωση

- Συναντήσεις Σπάρτης 1η

- Συναντήσεις Πατρών 1η

- Συναντήσεις Πατρών 2η και Σπάρτης 2η

- Συναντήσεις Πατρών 3η

- Συναντήσεις Πατρών 4η και Σπάρτης 3η

- Συαναντήσεις Πατρών 5η και Ειδική Εκδήλωση, Συναντήσεις Σπάρτης 4η και Εορταστικό Συμπόσιο

- Συναντήσεις Πατρών 6η, Σπάρτης 4η και Συμπόσιο Εορταστικό

- Συναντήσεις Πατρών 7η και Σπάρτης 5η

- Συνάντηση Πατρών 8η

- Συνάντηση Πατρών 9η και Σπάρτης 6η

- Συνάντηση Πατρών 10η και Ειδική Εκδήλωση 2η

- Συνάντηση Πατρών 11η και Σπάρτης 7η

- Συνάντηση Πατρών 12η

- Συνάντηση Πατρών 13η και Σπάρτης 8η

- Συνάντηση Πατρών 3η Ειδική και 14η Τακτική, Σπάρτης 9η

- Συνάντηση Πατρών 15η

- Συμπόσιο Εαρινής Ισημερίας και Συνάντηση Πατρών 16η

- Συναντήσεις Πατρών 17η, Σπάρτης 10η, Επετειακή και Αρχαιολογική Συνάντηση

- Σεμινάριο 18ο Πατρών και 11ο Σπάρτης, Ειδική και Αρχαιολογική Συνάντηση

- Συνάντηση Πατρών 19η

- Εγκαίνια Κέντρου Μεγαρικών Μελετών, 12η Συνάντηση Σπάρτης, Ειδική και Αρχαιολογική Συνάντηση

- Σεμινάριο 20ο Πατρών και 13ο Σπάρτης, Ειδική Εκδήλωση για το Παρελθόν και το Παρόν της Σπάρτης, Αρχαιολογική Συνάντηση

- Σεμινάριο 21ο Πατρών

- Σεμινάριο 23ο Πατρών

- Σεμινάριο 24ο Πατρών και 15ο Σπάρτης, Ειδική και Αρχαιολογική Συνάντηση

- Σεμινάριο 22ο Πατρών και 14ο Σπάρτης, Ειδική και Αρχαιολογική Συνάντηση

- Σεμινάριο 25ο Πατρών

- Έκτακτη Συνάντηση, Σεμινάριο 26ο Πατρών και 16ο Σπάρτης, Συμπόσιο και Ειδική Συνάντηση

- Σεμινάριο 27ο Πατρών, Χωρολογική και Αρχαιολογική Συνάντηση Αργολίδας

- Σεμινάριο 28ο Πατρών και Έκτακτη Συνάντηση

- Σεμινάριο 29ο Πατρών, Θερινή 1η Συνάντηση Σπάρτης, Συμπόσιο και Αρχαιολογική Συνάντηση

- Σεμινάριο 30ο Πατρών

- Σεμινάριο 31ο Πατρών

- Σεμινάριο 8ο Πατρών και 5ο Σπάρτης και δυο Εκδηλώσεις για την Αχρήματη και Άνομη Πόλη

- Σεμινάρια Πατρών ΛΓ' και Σπάρτης Δ'

- Πρόγραμμα Σεμιναρίων Πατρών ΛΓ' Κύκλος

- Πρόγραμμα Σεμιναρίων Σπάρτης Δ' Κύκλος

- Σεμινάριο 1ο Πατρών και 1ο Σπάρτηςκαι Εκδήλωση για την Ωραία Ελένη

- Σεμινάριο 2ο Πατρών

- Σεμινάριο 3ο και 4ο Πατρών και 2ο Σπάρτης και Εκδήλωση για τους Διοσκούρους

- Σεμινάριο 4ο Πατρών και Εκδήλωση για τον Απόλλωνα και τον Χριστό

- Σεμινάριο 5ο Πατρών και 3ο Σπάρτης Συμπόσιο και Εκδήλωση για τον γεννώμενο Παίδα

- Σεμινάριο 6ο Πατρών και 4ο Σπάρτης και δύο Εκδηώσεις στην Σπάρτη για τους Διαφορετικούς Δρόμους 3 Δωρικών Πόλεων και για την Σπάρτη και τα Μυστήρια

- Σεμινάριο 7ο Πατρών

- Σεμινάριο Έκτακτο για τον Απόλλωνα και τον Χριστό στην Ρωμαική Αυτοκρατορία

- Σεμινάριο 9ο Πατρών

- Σεμινάριο 10ο Πατρών και 6ο Σπάρτης και Ειδική Εκδήλωση για την Διαχείριση των Αναγκών του Χρόνου σε μια Κοινωνία της Τελειότητας

- Σεμινάριο 11ο Πατρών

- Σεμινάριο 7ο Σπάρτης, Συμπόσιο Γεωπολιτικής, και Ειδική Εκδήλωση για την Υψηλή Στρατηγική της Σπάρτης

- Σεμινάριο 12ο Πατρών και Μικρό σχόλιο για το Συμπόσιο Γεωπολιτικής στην Σπάρτη

- Σεμινάριο 13ο Πατρών και 8ο Σπάρτης και ειδική Εκδήλωση για Σπάρτη και Ασσυρία

- Σεμινάριο 14ο Πατρών

- Σεμινάριο 15ο Πατρών και 9ο Σπάρτης και ειδική Εκδήλωση για τον Ελληνισμό και τον Νεοελληνισμό.

- Σεμινάρια Πατρών και Σπάρτης - 24 Μαρτίου'

- Σεμινάρια Πατρών ' και Σπάρτης 31 Μαρτίου

- Σεμινάρια Πατρών ΛΓ' και Σπάρτης Δ' 8 Απριλίου

- Σεμινάριο Πατρών 19ο

- Σεμινάριο Πατρών 20ο

- Σεμινάριο Πατρών 21ο

- Σεμινάριο Πατρών 22ο

- Σεμινάριο Πατρών 23ο

- Σεμινάριο Πατρών 24ο

- Σεμινάριο Πατρών 25ο

- Σεμινάρια Πατρών 26ο και 27ο, και Σεμινάριο Σπάρτης 11ο και Ειδική Εκδήλωση

- Σεμινάριο Πατρών 28ο και Σεμινάριο Σπάρτης 12 με Ειδική Εκδήλωση

- Σεμινάριο Πατρών 29ο

- Σεμινάριο Πατρών 30ο, Σπάρτης 13ο και Ειδική Εκδήλωση

- Σεμινάριο Πατρών 31ο και Χωρολογική εκδρομή στον Θέρμο

- Σεμινάριο Πατρών 32ο Σπάρτης 14ο και Ειδική Εκδήλωση

- Σεμινάριο Πατρών 33ο και Χωρολογική Συνάντηση για τον Επικούριο Απόλλωνα

- Μεσοδιάστημα 2019

- Χωρολογικά Μεσοπεριόδου 2020

- Χωρολογική και Αρχαιολογική Συνάντηση στον Θέρμο, Αιτωλίας

- Χωρολογική και Αρχαιολογική Συνάντηση στην Ανδρίτσαινα για τον Επικούριο Απόλλωνα

- Συνάντηση της Σπάρτης για τα Υακίνθια και τις Γυμνοπαιδιές

- Συνάντηση της Σπάρτης για την Μάχη των Θερμοπυλών και τα Κάρνεια

- Συμπληρωματικό Σημείωμα

- Συνάντηση της Σαντορίνης Σεπτεμβριος 2020

- Συναντήσεις Πατρών ΛΔ' και Σπάρτης Ε'

- Πρόγραμμα Σεμιναρίων Πάτρας, Κύκλος 34ος

- Πρόγραμμα Σεμιναρίων Σπάρτης, Κύκλος Ε'

- Έναρξη Ε' Κύκλου Συναντήσεων Σπάρτης

- ΣΣεμινάριο Πατρών 1ο και Σπάρτης 2ο τριπλό

- Συναντήσεις Πατρών 2η

- Συναντήσεις Πατρών 3η και Διαδικτυακή Ομιλία στο Διεθνές Πλατωνικό Σεμινάριο, Πολωνία

- Συναντήσεις Πατρών 4η, 5η, Σπάρτης 3η και Παράλληλος Κύκλος

- Συναντήσεις Πατρών 6η, Α΄Χωρολογική Εκδρομή Αργολίδας

- Συναντήσεις Σπάρτης Μεσοπεριόδου, Β΄Χωρολογική Εκδρομή Λουσίου

- Συναντήσεις Σπάρτης μεσοπεριόδου 2η

- Κύκλοι 2022

- Συναντήσεις Πατρών ΛΔ΄ Κύκλος

- Συναντήσεις Σπάρτης Ε΄ Κύκλος Ελληνισμός και Ιστορία

- Συναντήσεις Σπάρτης Συμπληρωματικό Μέρος: Κριτική Ιστορία της Ελληνοπερσικής Σύγκρουσης

- Μορφή: η Αλήθεια και το Κάλλος της Σπάρτης

- Συναντήσεις Σπάρτης Φεβρουαρίου

- Πασχαλινό Πρόγραμμα

- Συναντήσεις Πατρών και Σπάρτης αρχών Μαίου

- Συνάντηση πατρών 19 Μαίου

- Συναντήσεις Πατρών και Σπάρτης τέλη Μαίου

- Συναντήσεις Πατρών αρχές Ιουνίου

- Η Χώρα του Αταίριαστου και Συναντήσεις Πατρών και Σπάρτης μέσα Ιουνίου

- Ο Φισικός Σπαρτιάτης και οι Απόσπαρτοι και Συνάντηση Πατρών τέλη Ιουνίου

- Συναντήσεις Πατρών και ΔΕΛΦΏΝ αρχές Ιουλίου

- Συναντήσεις Πατρών μέσα Ιουλίου και Συνέχεια από τους Δελφούς

- Συνάντηση Πατρών 21 Ιουλίου

- Συναντήσεις Πατρών, Σπάρτης και Λυκαίου, 28 Ιουλίου - 8 Αυγούστου

- Συναντήσεις Σπάρτης Σεπτεμβρίου και Διεθνές Συνέδριο

- Χωρολογικές Συναντήσεις 2022

- Συναντήσεις Πατρών Κύκλος ΛΕ' 2022-3

- Πρόγραμμα

- Σεμινάριο 1ο

- Σεμινάριο 2ο

- Σεμινάριο 3ο

- Σεμινάριο 4ο και 5ο Πατρών, 2ο τριπλό Σπάρτης

- Σεμινάριο 5ο Πατρών

- Σεμινάριο 6ο Πατρών

- Σεμινάριο 7ο Πατρών, 3ο τριπλό Σπάρτης, και 1ο Άργους

- Σεμινάριο 9ο και 10ο Πατρών, 4ο τριπλό Σπάρτης και 2ο Άργους

- Σεμινάριο 11ο Πατρών

- Σεμινάριο 12ο και 13ο Πατρών, 5ο τριπλό Σπάρτης και 3ο Άργους

- Σεμινάριο 14ο Πατρών

- Σεμινάριο 15ο και 16ο Πατρών, 6ο τριπλό Σπάρτης και 4ο Άργους

- Σεμινάριο 17ο και Βοιωτικά

- Σεμινάριο 18ο Πατρών

- Σεμινάριο 19ο Πατρών

- Σεμινάριο 20ο και 21ο Πατρών, 7ο τριπλό Σπάρτης και 6ο Άργους

- Σεμινάριο 22ο Πατρών

- Σεμινάριο 23 και 24ο Πατρών

- Σεμινάριο 25ο Πατρών

- Σεμινάρια 26ο και 27ο Πατρών

- Σεμινάριο 28ο Πατρών

- Σεμινάρια 29ο και 30ο Πατρών

- Συναντήσεις Σπάρτης Κύκλος ΣΤ' 2022-3

- Πρόγραμμα

- Σεμινάριο 1ο και Συμπληρωματικά 1ου

- Σεμινάριο 4ο και 5ο Πατρών, 2ο τριπλό Σπάρτης

- Σεμινάριο 7ο Πατρών, 3ο τριπλό Σπάρτης, και 1ο Άργους

- Σεμινάριο 9ο και 10ο Πατρών, 4ο τριπλό Σπάρτης και 2ο Άργους

- Σεμινάριο 12ο και 13ο Πατρών, 5ο τριπλό Σπάρτης και 3ο Άργους

- Σεμινάριο 15ο και 16ο Πατρών, 6ο τριπλό Σπάρτης και 4ο Άργους

- Σεμινάριο 20ο και 21ο Πατρών, 7ο τριπλό Σπάρτης και 6ο Άργους

- Σεμινάριο 8ο τριπλό Σπάρτης

- Σεμινάριο 9ο τριπλό Σπάρτης

- Σεμινάριο 10ο τριπλό Σπάρτης

- Συναντήσεις Άργους Κύκλος Α' 2023

- Σεμινάριο 7ο Πατρών, 3ο τριπλό Σπάρτης, και 1ο Άργους

- Σεμινάριο 9ο και 10ο Πατρών, 4ο τριπλό Σπάρτης και 2ο Άργους

- Σεμινάριο 12ο και 13ο Πατρών, 5ο τριπλό Σπάρτης και 3ο Άργους

- Σεμινάριο 15ο και 16ο Πατρών, 6ο τριπλό Σπάρτης και 4ο Άργους

- Πρόγραμμα Σεμιναρίων Άργους

- Σεμινάριο 5ο Άργους

- Σεμινάριο 20ο και 21ο Πατρών, 7ο τριπλό Σπάρτης και 6ο Άργους

- Σεμινάριο 7ο Άργους

- Σεμινάριο 8ο Άργους

- Σεμινάριο 8ο Άργους

- Χωρολογικές Συναντήσεις 2023

- Συναντήσεις Πατρών ΛΣΤ΄ και Σπάρτης Ζ΄

- Συναντήσεις Πατρών 2023-4 Πρόγραμμα

- Συαντήσεις Σπάρτης 2023-4 Πρόγραμμα Κύριο

- Συναντήσεις Σπάρτης 2023-4 Πρόγραμμα Παράλληλο

- Συναντήσεις Σπάρτης 2023-4 Πρόγραμμα Συμπληρωματικό

- Συνάντηση Πατρών 1η και Σπάρτης 1η

- Συνάντηση Πατρών 2η

- Συναντήσεις Πατρών 3η και Τέταρτη, και Σπάρτης 2η

- Συνάντηση Πατρών 5η

- Συαντήσεις Πατρών 6η και 7η και Σπάρτης 3η

- Συνάντηση Πατρών 8η

- Συναντήσεις Πατρών 9η και 10η και Σπάρτης 4η

- Χρονολογθκές Συναντήσεις

- Varia

- Greece a failed State in a failing "Europe"

- Liberalise and Open the Union and the States

- Neohellenism

- Το Νεοελληνικό Leviathan

- Το Νεοελληνικό Leviathan (Συνέχεια)

- Η Τριτη Επανάσταση

- Που Βρίσκεται η Αρρώστεια

- Οι Υποτελείς Μπακάληδες της Εξουσίας A

- Οι Υποτελείς Μπακάληδες της Εξουσίας Β

- Ποιος και Γιατί να Επενδύσει σε μια Αποτυχημένη Χώρα;!

- Το Νεοελληνικό Ζήτημα

- Η Αναξιοπιστία του Νεοελληνικού Leviathan

- Τι Θέλει το Σύστημα και Γιατί

- Φιλοσοφία και η Παγκόσμια Οικονομική Κρίση

- ΤΟ ΕΙΔΩΛΟ ΤΟΥ ΚΡΑΤΙΚΟΥ ΠΑΡΕΜΒΑΤΙΣΜΟΥ ΣΤΗΝ ΟΙΚΟΝΟΜΙΑ

- Επι πρωτου ετους της χρεωκοπιας

- Σχέδια Διάσωσης του Leviathan (και των Πιστωτών του) ή Στρατηγική Ανάταξης της Χώρας;

- ΕΚΛΟΓΕΣ 2010 Ο ΘΡΙΑΜΒΟΣ ΤΗΣ ΑΠΟΧΗΣ ΤΩΝ ΔΗΜΙΟΥΡΓΩΝ

- ΕΜΠΡΟΣ ΣΤΗΝ ΑΡΧΗ

- Απο τα Είδωλα του Leviathan: Αντιδραστικό Στρατηγικό Δόγμα

- ΟΙ ΕΚΛΟΓΕΣ ΕΙΝΑΙ ΜΕΡΟΣ, ΚΑΙ ΟΧΙ ΛΥΣΗ, ΤΟΥ ΠΡΟΒΛΗΜΑΤΟΣ

- TΟ ΣΥΣΤΗΜΑ ΠΑΕΙ ΕΚΛΟΓΕΣ

- Το Μήνυμα των Εκλογών

- Η ΚΟΙΝΩΝΙΑ ΔΙΑΓΡΑΦΕΙ ΤΟ ΣΥΣΤΗΜΑ - ΚΑΙ ΓΙΑΤΙ

- Η ΜΑΤΑΙΗ «ΜΕΤΑΡΡΥΘΜΙΣΗ» ΤΟΥ ΚΑΤΑΡΡΕΟΝΤΟΣ ΚΑΘΕΣΤΩΤΟΣ

- Η ΑΛΗΘΕΙΑ ΓΙΑ ΤΗΝ ΚΑΤΑΣΤΑΣΗ ΤΗΣ ΧΩΡΑΣ

- Η ΜΑΤΑΙΗ «ΜΕΤΑΡΡΥΘΜΙΣΗ» ΤΟΥ ΚΑΤΑΡΡΕΟΝΤΟΣ ΚΑΘΕΣΤΩΤΟΣ Β'

- Η ΕΥΚΑΙΡΙΑ ΑΙΩΝΩΝ ΚΑΙ Η ΚΑΤΑΣΤΡΟΦΗ ΤΗΣ ΧΩΡΑΣ ΑΠΟ ΤΟ ΚΑΘΕΣΤΩΣ LEVIATHAN

- Γιατί η Έξοδος από τον Λαβύρινθο περνάει από το Σκότωμα του Μινώταυρου

- Λόγος για τους Εθνικούς Ευεργέτες

- Ελευθερία και Πολιτιστική Ταυτότητα

- Η ΚΟΥΤΟΠΟΝΗΡΙΑ ΤΟΥ LEVIATHAN

- Η Γεωπολιτική του ΒαλκανοΜικρασιατικού Χώρου και οι Πόζες του Leviathan

- H Ευρωπαική Ενωση δεν ειναι Ενωση αλλα μια Συμμαχία με Θολές Αρχές

- Πρωτοχρονιάτικες Αρές

- Πάτρα: Πολιτισμός Ώρα Μηδέν

- Ο Λαβύρινθος, η Κόπρος του Αυγεία και ο Γόρδιος Δεσμός

- Οι Αρκούδες των Αρκουδιάρηδων

- Η Εκδίκηση του Πνεύματος: Μια Χώρα χωρίς Ταυτότητα Βουλιάζει

- Παίρνουν Ναρκωτικά...

- In rebus trepidis ultimum consilium

- Τα Όρια της (Αν)αξιοπρέπειας και τα Όρια της Κουτοπονηριάς

- Κρίση Ταυτότητας του ΝεοΕλληνισμού: και Πρώτα στο Πολιτειακό

- Εμπρός στην Αρχή: Σκοτώνοντας Πρώτα τον Μινώταυρο

- Τριτοκοσμική Κουλτούρα και "Μητροπολιτικό Θέατρο"

- ΕΛΛΗΝΙΚΕΣ ΑΞΙΕΣ ΚΑΙ ΝΕΟΕΛΛΗΝΙΚΕΣ ΑΠΑΞΙΕΣ

- Η ΛΟΓΙΚΗ ΤΗΣ ΠΡΑΓΜΑΤΙΚΟΤΗΤΑΣ ΚΑΙ Ο ΠΑΡΑΛΟΓΙΣΜΟΣ ΤΟΥ ΚΑΘΕΣΤΩΤΟΣ

- Οι Ιδιωτικοί Οίκοι Αξιολόγησης και οι Πολιτικές Εξουσίες

- Η Επανάσταση του Ελληνισμού

- Η Αρώστεια της Ηγετικής Αναξιοκρατίας

- Αρχές Νέας Πολιτειακής Συγκρότησης

- Η Ασυνέχεια της Νέας Αρχής: ειδωλοκλασία και ελευθρρία

- Τα Πάθη και η Ανάσταση του Υιού του Ανθρώπου

- Ο Πολιτισμός του Νέου και ο Βαρβαρισμός του Παλαιού

- "Το πιό φριχτό ναυάγιο θα ήταν να σωθούμε"

- Το Αναπόφευκτο και τα Ευρωζωνικά Μπερδέματα

- ΓΙΑΤΙ;

- Ζήτω η 28 Οκτωβρίου 2011: Η Δόξα της Κοινωνίας και η Βδελυρία του Καθεστώτος Υποτέλειας

- Από το Δημοψήφισμα της Κυτοπονηριάς στον Πανικό της Κυβέρνησης Συμφωνημένης Μειοδοσίας

- Ώδινεν όρος και έτεκε μυν: το Καθεστώς βρήκε την Ρόμπα του

- 'Ολα τάχει η Μαριορή κι ο Φερετζές της λείπει

- Η Ατιμωτική για την Ελλάδα Συνεύρεση

- Ελληνικό Μάθημα προς την Καγκελλάριο της Γερμανίας

- ΟΧΙ!

- Θεατρική Κριτική

- Ο θάνατος του Εμποράκου

- Η Ασχημια Της «Ασχημης Αδελφης»

- Ασχημη Αδελφη - Ιντζεγιάννης

- Ασχημη Αδελφη - Δημητρόπουλος

- Παράλληλοι Στοχασμοί

- Η Τραγωδία της Τραγωδίας

- «ΟΙΔΙΠΟΥΣ ΤΥΡΑΝΝΟΣ» ΤΟΥ ΣΟΦΟΚΛΗ ΑΠΟ ΤΟ ΑΜΦΙ-ΘΕΑΤΡΟ: ΜΕΤΡΟ ΚΑΙ ΜΕΤΡΙΟΤΗΤΑ

- Arthur Miller, A View from the Bridge

- Κατάντιες!

- Ο "Ηρακλής Μαινόμενος" του Ευριπίδη και μια τρελή παράστασή του

- Ανάλυση και Πρόγνωση: Αρθρα 2000-2001

- Μαθημα Στρατηγικής

- Ο Φετιχισμός του Status Quo

- Ο Ελληνισμός και η Ολοκλήρωση του ΒαλκανοΜικρασιατικού Πεδίου

- Βιώσιμη Λύση του "Γιουγκοσλαυικού" Ζητήματος

- Ο Ευρωπαικός Εθνικισμός αποσταθεροποιεί το ΒαλκανοΜικρασιατικό Πεδίο

- Ευρωπαιστικός Αναχρονισμός

- Η Ώρα της Αλήθειας για τους Ευρωπαιστές

- Κράτος - Πλαίσιο

- Η Ένταξη της Χώρας στην ΟΝΕ

- Παγκοσμιοποίηση Ή Ευρωπαισμός;

- Η Παθολογία της ΝεοΕλληνικής Παρακμής

- Πολυμερισμός των Προβληματικών Περιοχών

- Ο Ρεαλισμός τησ Νέας Αμερικανικήσ Στρατηγικής Απελευθερώνει το Παγκόσμιο Σύστημα

- Η Ορθόδοξη Πνευματικότητα και η ΦιλοΔυτική Πολιτική

- Ο Πάπας και η Ευρωπαική Τεχνητότητα

- Πραγματική Σταθεροποίηση

- Τί Φταίει;

- Προβληματικές Επιχειρήσεις και Προβληματική Εθνική Οικονομία

- Ο Πραγματικός Εκσυγχρονισμός του ΝεοΕλληνισμού δεν Περνάει από τον Εξευρωπαισμό του

- Αμερικανικές Εγγυήσεις και Ευρωπαική Ολοκλήρωση

- Ο Ευρωπαικος Εκβιασμός και η Νέα Φάση της Αμερικανικής Στρατηγικής

- Αστάθεια ή Φυσική Τάξη;

- Η Υποβάθμιση μιας Χώρας σαν Συνέπεια Στρατηγικών Σφαλμάτων της Ηγεσίας της

- Η Ανίσχυρη "Ιερά" Συμμαχία

- Το Επικίνδυνο Ευρωπαικό Παιχνίδι

- Οι ΗΠΑ από την Ηγεσία της Δύσης στην Παγκόσμιο Ηγεμονία

- Η Φυσική Τάξη ενός Ελεύθερου Συστήματος ειναι η Μόνη Ευσταθής και Μαξιμαλιστική

- Συνεντεύξεις και Δημοσιεύσεις σε ΜΜΕ για την Παγκόσμιο Οικονομική Κρίση

- Γιατί η κρίση ήταν και ορατή και προβλέψιμη

- Κριτική της Κριτικής των Αγορών και η Σημασία της Παγκοσμιοποίησης

- Η Παγκόσμια Οικονομική Κρίση και η Κρίση της Ευρώπης

- Ευρωπαική Ματαιότης Ματαιοτήτων

- ΤΟ ΕΙΔΩΛΟ ΤΟΥ ΚΡΑΤΙΚΟΥ ΠΑΡΕΜΒΑΤΙΣΜΟΥ ΣΤΗΝ ΟΙΚΟΝΟΜΙΑ

- Η ΔΙΑΡΡΟΗ ΑΠΟΡΡΗΤΩΝ ΑΜΕΡΙΚΑΝΙΚΩΝ ΔΙΠΛΩΜΑΤΙΚΩΝ ΕΓΓΡΑΦΩΝ ΣΤΟ ΔΙΑΔΙΚΤΥΟ

- Κριτική της Κριτικής των Αγορών και η Σημασία της Παγκοσμιοποίησης (Κριτική των Θέσεων του Padoa-Schioppa

- Critique of Soros' Philosophy of Economy

- Contemporary Historical Developments and Strategy

- Η Υψηλή Στρατηγική των Η.Π.Α.

- ΟΙ Πολιτιστικές Παράμετροι της Ιστορίας

- Το Χρήμα και η Πραγματική Οικονομία

- State - Religion Relationships

- Η Εξέλιξη του Συσχετισμού Ισχύος στο Παγκόσμιο Σύστημα τα Τελευταία 100 Χρόνια

- Ο Αιώνας της Ελευθερίας

- Το Οικονομικό Πρόβλημα των ΗΠΑ

- Προς την Φυσική Λύση του Ανατολικού Ζητήματος

- ΤΕΡΜΑ ΤΑ ΨΕΜΜΑΤΑ ΚΑΙ ΤΕΛΟΣ ΕΠΟΧΗΣ

- Για την Φυσική Λύση του Ανατολικού Ζητήματος

- Πολιτική και Οικονομία στον 21ο Αιώνα - 2

- Regional Geodynamics in the Balkan-Asia Minor Field

- Bulgaria's Lesson on Euro-madness

- Oxyrhynchus Papyrus 4941 OxyLXIII

- Για την Πάτρα

- "ΠΑΤΡΙΝΟ ΚΑΡΝΑΒΑΛΙ"

- Πως να δημιουργήσουν Πολιτισμό όταν δεν ξέρουν να αξιοποιήσουν Θησαυρό;

- Τριτοκοσμική Κουλτούρα και "Μητροπολιτικό Θέατρο"

- Πάτρα: Πολιτισμός Ώρα Μηδέν

- Το Μήνυμα των Εκλογών και η Πάτρα

- Η Υποκουλτούρα της Χαμοσύνης

- Το Γνήσιο και το Ψευδεπίγραφο ή πως η Νεοελληνική Επισημοκρατία σκοτώνει

- Θέατρο και Μουσική σε ένα Μητροπολιτικό Δήμο

- ΤΕΛΟΣ ΕΠΟΧΗΣ¨Έξω οι Παρέεσ και η "Λογική" τους

- ΚΑΙ ΠΑΛΙ Ο ΠΟΛΙΤΙΣΜΟΣ ΚΑΙ Η ΧΑΜΟΣΥΝΗ

- Δημόσια Διαβούλευση για το Θέατρο!

- Η Πάτρα αποπολιτίζεται (2006)

- Gurob Papyrus

- A.L.Pierris: Ergography (Published Works)

- List of Publications

- Η Μοναδική Σωτηρία για την Ελλάδα

- Η Μία και Μοναδική Σωτηρία

- Οικονομική Λογική και Πολιτική Παράνοια

- Ανατομία της Μειοδοσίας

- Η Φαυλικρατία, οι Ξένοι και Εμείς

- Τί συμφέρει την Χώρα (και Όχι το καθεστώς)

- Οικονομική Σωτηρία της Ελλάδας: η Μοναδική Οδός

- Η Μοναδική Οδός Σωτηρίας της Κοινωνίας και της Χώρας

- Η Αιτία του Εγκλήματος Καθοσιώσεως του Καθεστώτος κατά της Ελλάδας: Ευρωπαισμός

- Ευρώ: Πρόγνωση και Εξελίξεις

- Σχέδιο Πολιτιστικής Δράσης

- Αγιογράφηση Αγίου Ανδρέου Πατρών

- Πρόταση για μια Νέα Τοπική Ιστορία

- Ανάλυση Και Πρόγνωση 2 : Άρθρα 2002

- Η Φύση της Σύγχρονης Τρομοκρατίας και ο Πόλεμος Εναντίον της

- Η Γεωστρατηγική του Ελληνικού Χώρου

- Το Αδιέξοδο του Φονταμενταλιστικού Ευρωπαισμού

- Τα Πολιτικά Αίτια της Οικονομικής Αποτυχίας στην Αργεντινή

- Η Άρνηση του Κατεστημένου να κάνει Απελευθέρωση στην Αργεντινή εντιν

- Η Δημοκρατία στην Ελλάδα ειναι Αβαθής

- Ουσία της Δημοκτατίας ειναι η Ελευθερία

- Καλύτεροι κανόνες ειναι οι Λιγώτεροι και Φυσικώτεροι

- Αντιδημοκρατικός Παρεμβατισμός της Πολιτικής Εξουσίας στις Ένοπλες Δυνάμεις

- Η Στρατηγική των "Διεθνών Κανόνων Δικαίου" ειναι απλώς Υποκριτική και Λανθασμένη Στρατηγική Συμφερόντων

- Χρειαζόμαστε τώρα την Επανάσταση της Απελευθέρωσης περισσότερο από ό,τι το 1821

- Η Αναξιοκρατία ειναι η Καθαρή Τυραννία

- Ατομική Δημιουργική Δράση Ενάντια στην Θεσμική Δυσλειτουργία και Έξω από αυτήν

- Η Παρακμή και το Τέλος των Θεσμών από την Αναξιοκρατία των "Καρεκλούχων" τους

- Πόλεμος και Ειρήνη: Ευσταθής Ισορροπία ειναι μόνον η Ελεύθερη και Φυσική

- Η ΠΟλιτική Σύγχυση στην Ελλάδα

- Η Πραγματικότητα της Παγκοσμιοποίησης και οι Ουτοπίες του Οικουμενισμού και του Ευρωπαισμού

- Οι Απειλές του Μέλλοντος

- Ανατομία της Νεοελληνικής Αποτυχίας

- Η Αναξιοπιστία της Ελληνικής Εξωτερικής Πολιτικής και Πολιτικής Ασφάλειας α

- Η Ελληνική Εξωτερική Πολιτική δεν εκφράζει την Γεωστρατηγική του Οικείου Χώρου μας

- Απόλυτη Στρατηγική Προτεραιότητα ο Συνολικός ΕλληνοΤουρκικός Συντονισμός

- Ο Αναλλοίωτος Αναχρονισμός του ΝεοΕλληνικού Καθεστώτος

- Η Μωρή Εξωτερική Πολιτική του Καθεστώτος της Χώρας

- Για την Ανάσταση του Ελληνισμού

- Η ΝεοΕλληνική "Κουλτούρα" της Φαυλοκρατίας

- Τα Λάθη Πληρώνονται - και Ειναι Δίκαιο

- Analysis and Forecasting: Greece a Failed State

- Εκλογές 6ης Μαίου 2012

- Εκλογές 17ης Ιουνίου 2012

- Εκλογές 25 Ιανουαρίου 2015

- Μανιφέστα 2015

- Ι. Πρόσω ολοταχώς: Ριζοσπαστική Στρατηγική για την Αναγέννηση της Ελλάδας

- ΙΙ. Εμπρός! Να Γκρεμίσουμε την Ελλάδα που Μας Πληγώνει

- ΙΙΙ. Καθαρά Λόγια

- IV. Ο "Μέγας Ασθενής" και η Ελλάδα

- V. Εθνική Ανεξαρτησία ή Ευρωπαικό Προτεκτοράτο;

- VI. Υπερήφανος Επαίτης δεν Υπάρχει - ούτε Αξιοπρεπής Πίθηκος

- VII. Η Ευρωπαιστική Ιδεοληψία και οι Κυβερνήσεις του Εσωτερικού Καθεστώτος Καταπίεσης της Ελλάδας

- VIII. Γιατί Γελάμε με τον Παλιάτσο κι όταν Κλαίει

- IX. Ευρωπαισμός: το Ανθελληνικό Στρατηγικό Δόγμα του Καθεστώτος Εσωτερικής Κατοχής της Χώρας

- X. Σταράτα Λόγια

- XI. "Γνώθι σαυτόν": το Νόημα της Επανάστασης - τί Εορτάζουμε Σήμερα/// Επαιτεία και Επωδές/// Η Λογική του Εθνικού και του Κοινού Νομίσματος

- XII. Το Περί Γέλωτος Κράτος

- ΧΙΙΙ. Άπαξ Έτι! Ή Για Γέλια και Για Κλάματα

- ΧΙV. Οι Έσχατες των Ημερών

- XV. Πότε και Πώς Θα Γίνει Αυτό που Θα Γίνει;

- XVI. Ο Γόρδιος Δεσμός δεν λύνεται, Κόβεται!

- XVII. Οι Δυσθάνατοι, οι Εθελόδουλοι - και οι Εθελόκακοι

- XVIII. ΟΧΙ! Δεν Είμαστε σαν Αυτούς! - Έλληνες, Γραικύλοι και Παρακμιακοί Ευρωπαίοι

- XIX. : ΟΧΙ! Ο Θρίαμβος του Ελληνισμού και ο Εξευτeλισμός των Γραικύλων

- X. Παράνοια και Προδοσία Ή Οι Πρωθυπουργοί της Κωλοτούμπας

- ΧΧΙ. ΚΑΙ ΠΡΟΔΟΤΕΣ ΚΑΙ ΜΩΡΟΙ! Το Καθεστώς της Χώρας στα Απόνερα της Ιστορίας

- ΧΧΙΙ. Η Δύναμη της Αλήθειας, η Προπαγάνδα του Καθεστώτος και η Επανάσταση των Νέων

- ΧΧΙΙΙ. Ανθελληνισμός και Αφελληνισμός: η Πολιτική του Καθεστώτος υπέρ του Ευρωπαισμού

- XXIV. ΤΙ ΦΤΑΙΕΙ; Μονόδρομος για την Ελλάδα η Έξοδος από την Ευρωζώνη. - Ο Καθεστωτικός Ευρωπαισμός, Αιτία της Κακοδαιμονίας μας

- XXV. Για την Επανάσταση της Αυτογνωσίας

- ΧΧVI. Έλληνες και Γραικύλοι Ή Ο Fallmerayer δικαιώνεται από το Καθεστωτικό Κατεστημένο της Χώρας

- XXVII. Ελληνικές Σκέψεις για τις Καθεστωτικές Εκλογές της 20ης Σεπτεμβρίου

- Μανιφέστο ΧΧVIII:Post Mortem! Δεύτερες Ελληνικές Σκέψεις για τις Καθεστωτικές Εκλογές της 20ης Σεπτεμβρίου

- Μανιφέστα 2016

- Ένα, Δύο, Τρία... και ο Δημιουργικός Όλεθρος

- Ανδριάντες και Ανδρείκελα

- Ανεπηρέαστες Σκέψεις για το 1776 και το 1821

- Λεσβιακά: Αγαθή Μωρία ή Παιδαριώδης Πανουργία; Ιδού η Απορία - Τί θέλει η Δυτική Αλεπού στη Λέσβο με τον Σφραγιδοφύλακα εξ Ανατολών και τον Κρατικό Αξιωματούχο Εκκλησιάρχη παρουσία της Πολιτικής Ηγεσίας μιας Αποτυχημένης Πολιτείας;

- Νεοελληνικός Ιός

- Εκλογές 25 Ιουνίου 2023

- Greece a failed State in a failing "Europe"

{kind=link}

|

|

|

Apostolos L. PierrisBulgaria’s Lesson on Euro-madness

[A comment on the Wall Street Journal editorial of September 5, 2012, entitled “Bulgaria’s Lesson for Euro-Skeptics”].

One. The perverse idea that money is an independent variable in an economic system and that it consequently could be manipulated (with the best no doubt, if silly, intentions) by governments via their Central Bank subsidiaries is a barbaric conception of a barbarous century – that 20th century that marked the end of the European era in history with an eruption of end-of-time phenomena, complete with inhuman, utopian, eschatological ideologies, experimental and “modernistic” art, moral and religious confusion, the retreat of genuine philosophy, existentialism and Keynesianism, collapse of the nationalistic state and all-out wars the like of which (in size and kind) mankind had never before suffered.Some relics of the economic barbarism still remain under the masque of populist policies that enervate the individual’s creative activity and thus impede the intensification and full sway of economic dynamism. But there is all the same going on an irrevocable reversal back to classical (in all senses) theory including adequate recognition of the validity of the law of monetary-real economic interaction. The amount and “easiness”, the value and rate of interest, the financial means more generally, available in a given economy at a given state, are dependent on the volume, nature and nexus of human activity. There is a natural amount of money and a natural rate of interest for every system of free economy, that are in equilibrium to the mass, intensity (and reasonable expectation of growth) of human activity. That is what a sound monetary policy is all about. Two. It follows from One, that the only appropriate system of exchange rates in free economies is the floating one. Quite simply, the internal and external value of money should be left to be equated by the ineluctable and flawless and rational market forces both ways.The main rationale behind the urge to the adoption of a fixed exchange system regime is that it enforces necessary discipline (monetary and fiscal) on the governments of weaker, less competitive national economies. But a hugely better, more efficient and overall less costly correction is effected by simply letting them to drown under the ocean of their own people’s rage at their incompetence and at the consequent national failure. Three. A currency pegged to another is a special case of a fixed exchange rate regime. A currency board enhances the discipline introduced through the pegging by requiring that every monetary unit should be fully covered by appropriate reserves in the Central Bank of the country in question. All this can be easily achieved without any pegging and boarding – as it used to be done, say by the rigorous principle of convertibility to gold in the days of the gold standard.A currency union is the highest absurdity in the barbaric economic theory of the 20th century. It implies the same value and interest, hence volume and easiness, of money across disparate economies. If two economies are similarly structured and with similar prospects of development, then they may be joined together in a monetary union provided (and this as a huge “provided”) they both belong to the same geopolitical field and share the same geostrategic interests to such an extent that they may be willing to abandon to an essential degree their political independence and sovereignty. Such a combination of factors is extremely rare. In fact all significant monetary unions in history are consequent upon a war that integrates congenial spaces in a new state, thereby wielding a common interest among the variant members. Even this is an extraordinary event in human affairs. Four. Kremlin is an odd bedfellow to freedom, but truth is stronger than repression. Russia Today is absolutely right when it does (suit itself to) suggest that the Euro “grand design is deeply flawed, it’s built on sand, it’s a catastrophe”.Just that. Euro is a unique historical experiment in disastrous futility, it goes against the groin of all economic and political logic, it is sheer folly. The cart of a common currency with a centrally determined monetary policy has been put before the horse of state creation. Naïve or venal ideologues conceived of the Euro-zone as a building stone towards political integration, thus reversing the natural order of things. Common money is a manifestation of a common country, not a means towards it. Each national economy requires its own national currency. |